By Lisa Thompson

NASDAQ:IDBA

READ THE FULL IDBA RESEARCH REPORT

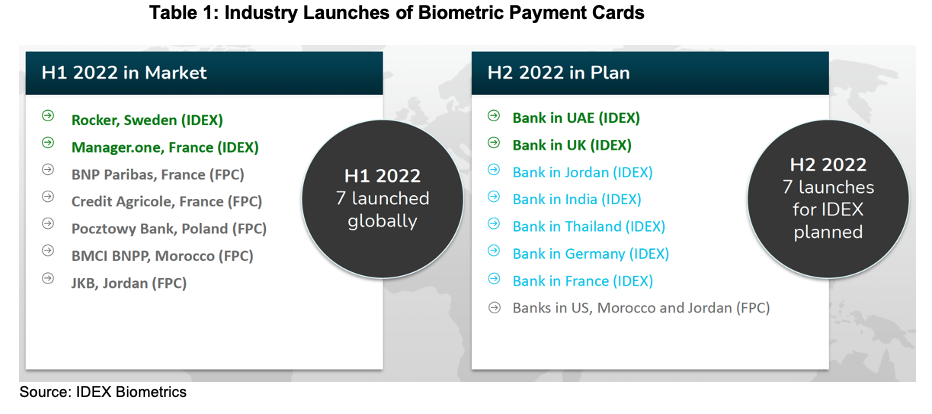

The second half of 2022 is finally seeing card launches around the world and IDEX (NASDAQ:IDBA) is seeing production orders for payment cards as well as for digital access. Most of the payment card launches are through IDEMIA and include banks in France, Jordan, India, Thailand, and the UK. IDEX expects ten launches of cards by the end of the year. The biggest payment card order landed to date is with First Abu Dhabi Bank which has three million members and is offering the card to all of them immediately. Cardholders do not have to wait until their current card expires but can get a fingerprint card on request. Fifteen percent of their members have already requested a new card and given that the lead time for IDEX is twelve weeks, we assume IDEMIA is already filling orders to go to FAB. Three million cards at a price of $3-4 per card yields revenues of $9-12 million for that one bank alone. Since IDEMIA is the go-between and it has at least eight other customer launches, it is hard for IDEX to know exactly what the uptake is and when at FAB, but it is certainly a better situation than the typical rollout which replaces members’ cards as they expire.

IDEMIA has landed two very large banks in France, which could be relatively huge near-term revenue generators. One has been in a pilot since April and will roll out to premium customers first, while the other has no premium customers and will roll out to its entire member base. We expect announcements very soon.

We also expect to see a card issued by a UK bank that could be or include a prepaid card that could be reloaded. There has been a lot of interest in this as a way to give kids (and those trying to control spending) money to spend that cannot be used by anyone else.

While IDEX does have interest from a US card manufacturer, that company has put its offerings on hold. However, payment cards are starting to be issued around the world with all of the activity being outside the US--as it was with chip and PIN adoption. Fortunately, this time there is no change of hardware needed on the retailer side. With only two providers—IDEX and Fingerprint Cards---it is easy to track the industry announcements around the world as shown in the table below.

IDEX expects ten launches of payment cards this year, or by early 2023 with four already announced. The four announced are Rocker, Manager.one, fidor, and First Abu Dhabi Bank (FAB). The ten are the total combined from Zwipe, banks and issuers, and via IDEMIA. At least six more new launches are anticipated in the fourth quarter of 2022.

Some customers are coming through Zwipe. Zwipe’s partners and customers include fidor, the national bank of Iraq, Legic, Placard, Wisecard, Qatar Fintech Hub, Modular, SCS Jordan, Mediterranean Bank, K2, and Mansour Bank. According to its Q3 report, Zwipe has seven pilots in the works with more coming. Revenue expectations for 2022 revenues are NOK$4 million and NOK$52 (US$5.1 million) in 2023.

IDEX is Signing Many Security Access Vendors at Higher Margins

While card volumes are large, margins on chips sold to the access security and cryptocurrency wallet market are much higher and have a faster sell cycle. Where IDEX may get $4 a card for a payment card, security application providers may pay $14-$50 a device for the same thing. That customer can then sell his product for much more. These customers will bring IDEX's gross margin above the 30% expected for payment cards. Providing physical security and preventing cybersecurity breaches are not focused on costs but on the ability to prevent very expensive losses. In addition, selling is mostly to a Chief Security Officer, not IT or a CEO making the selling cycle much shorter.

As a fabless semiconductor company with high operating leverage, it is expected to be at very high pretax margins once it ramps revenues and it deserves an enterprise value to sales valuation in line with its peers that trade at 6.3 times 2022 revenues. It currently trades at a $93 million market cap and an $83 million enterprise value. We believe that by 2025 it has the potential of $500 million in sales at which point it could be valued as a $3.7 billion company.

SUBSCRIBE TO ZACKS SMALL CAP RESEARCH to receive our articles and reports emailed directly to you each morning. Please visit our website for additional information on Zacks SCR.

DISCLOSURE: Zacks SCR has received compensation from the issuer directly, from an investment manager, or from an investor relations consulting firm, engaged by the issuer, for providing research coverage for a period of no less than one year. Research articles, as seen here, are part of the service Zacks SCR provides and Zacks SCR receives quarterly payments totaling a maximum fee of up to $40,000 annually for these services provided to or regarding the issuer. Full Disclaimer HERE.