By Steven Ralston, CFA

OTCQX:DYLLF | ASX:DYL

READ THE FULL DYLLF RESEARCH REPORT

SUMMARY OF RECENT EVENTS

- Advancement/De-Risking of flagship Tumas Project

- CEO Transition from John Borshoff to Greg Field

- Drilling Results at the S Bend and Tinkas Prospects

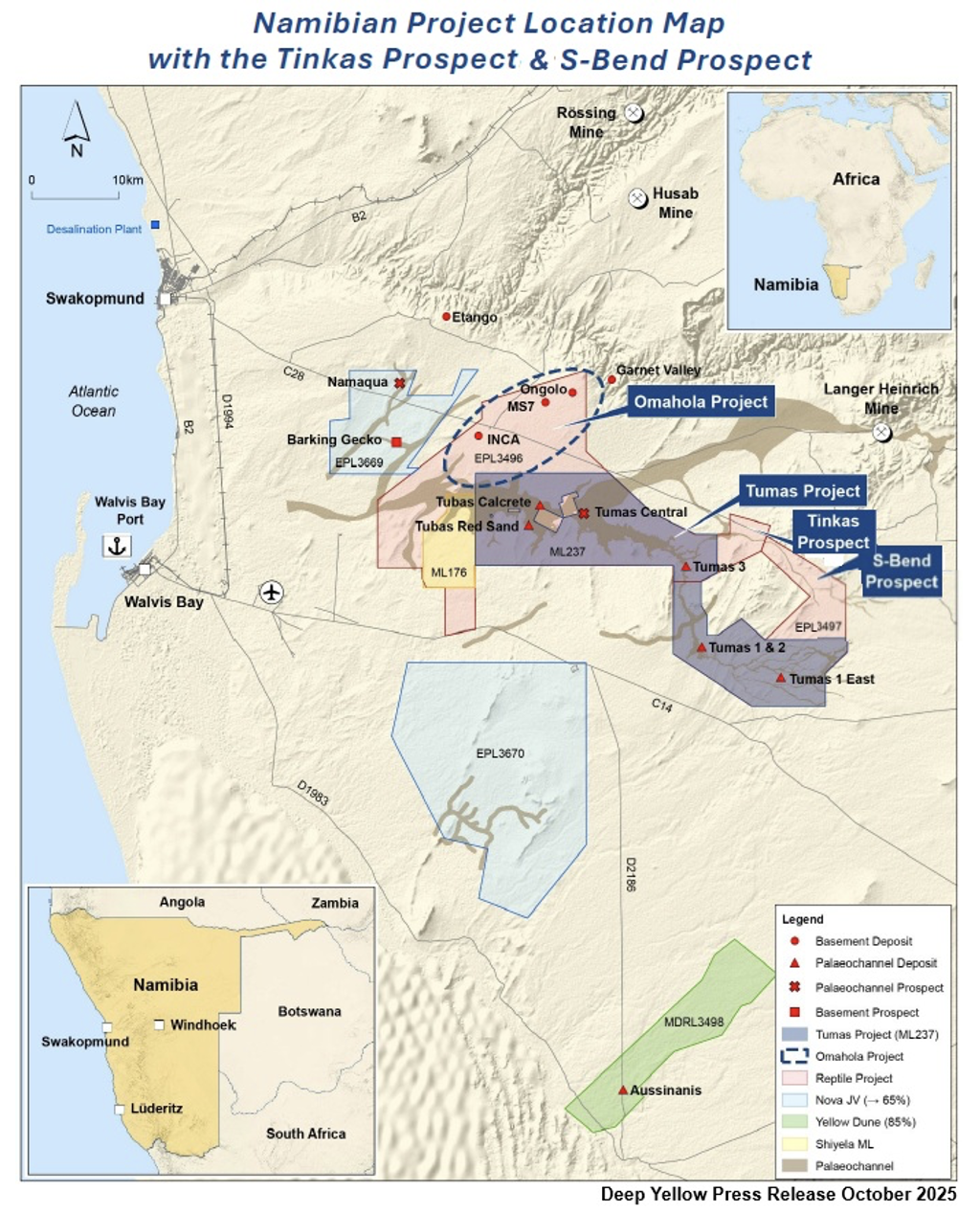

Tumas Project

Strategically, management is utilizing FID deferral period by further derisking the Tumas project through quantifiable progress across critical pre-production work streams. Over the last four months, detailed engineering has advanced from 44% to over 60% completion (with the 3D engineering model over 65% complete); procurement has progressed to over 70% of major equipment tendered compared to partial advancement in July, and orders for vendor data have been placed on all long lead equipment.

The most significant milestone was execution of the Power Supply Agreement with NamPower (subject to FID). The agreement defines a 22 km, 220 kV dedicated power line supplemented by solar BOOT (Build, Own, Operate and Transfer) arrangement targeting 30%+ of power requirements. Water supply agreements with NamWater advanced to draft stage with tenders received for the 65 km pipeline. Early works transitioned from planning to execution, with bulk earthworks having commenced in October 2025 with 24% completion attained as of December 17th with completion anticipated in March 2026.

On the project debt financing front, the Independent Technical Expert's environmental and social due diligence report has been completed laying the groundwork for the documentation phase for debt financing to commence.

Management continues to effectively execute on its staged development strategy in order to position the Tumas Project for rapid commencement of the construction phase once the uranium market supports the economics for initiating this greenfield project. Management continues to target 3Q of calendar 2027 for first production from Tumas.

Leadership Transition

On October 20, 2025, the Board of Directors of Deep Yellow (OTCQX:DYLLF) (ASX:DYL) announced the departure of CEO John Borshoff. Over the ensuing 6 market days, the shares of Deep Yellow declined 33% as many investors who considered the expertise and experience of John Borschoff as key factors in their investment decision process. No official announcement by the Board or John Borshoff has been made in order to clarify the rationale for Mr. Borshoff’s departure.

On December 2, 2025, the Board of Directors appointed Greg Field as CEO commencing no later than May 1, 2026 (due to a non-compete obligation). Rather than speculating on the situation or the motives of the parties involved, this transition of leadership could represent an evolution aligned with project lifecycle requirements. Noticeably, it is not an equivalent replacement. There is no dispute that Mr. Borshoff's five-decade uranium career (including the founding Paladin Energy and the development & operation of the Langer Heinrich mine), provided profound uranium-specific expertise during the initial development stage of Deep Yellow as a junior mining.

Mr. Field brings complementary production and operating mining capabilities rather than equivalent uranium experience relative to John Borshoff. Mr. Field has extensive considerable execution skills and considerable experience in multiple large-scale resource projects, including the Oyu Tolgoi copper & gold underground project in Mongolia, the Rincon lithium processing plant in Argentina and the AP60 aluminum smelter in Canada. However, the most notable distinction is the apparent lack of direct uranium mining experience, particularly low grade paleochannel uranium deposits of the Tumas Project and the lack of personal contacts within the Namibian mining industry. Nevertheless, mitigating factors include Deep Yellow’s technical team collective uranium experience, the advanced stage of the Tumas Project, and specialized uranium processing expertise of the EPCM contractor, Ausenco.

Drilling Results at the S-Bend Prospect

On October 14, 2025, Deep Yellow announced drilling results of a 452-hole (3,361 m) RC drilling programat the S-Bend Prospect located within the Exclusive Prospecting License 3497 and

situated adjacent to the north of Tumas 1 East. The drill program was designed to test approximately 4 km of the prospective shallow tributaries previously identified by previous limited drill testing. Drilling commenced on July 9th and concluded on September 22nd.

The best intersections include 8m at 332 ppm (SB0247), 2m at 1,217 ppm (SB0560), 5m at 407 ppm (SB0147), 5m at 367 ppm (SB0156) and 4m at 378 ppm (5m at 407 ppm (SB0282). The higher-grade mineralization was isolated to four main clusters. Further detailed drilling is required in order to delineate a resource that is associated with these clusters.

Drilling Results at the Tinkas Prospect

On October 30, 2025, Deep Yellow announced drilling results of a 105-hole (1,137m) RC drilling programat the Tinkas Prospect located within the Exclusive Prospecting License 3496 and

situated adjacent to the east of Tumas 3. The drill program was designed to test a radiometric surface anomaly initially identified by airborne electromagnetics. The is recognized to be a set of paleochannels that are tributaries of the main Tumas paleochannel. Drilling commenced on September 23rd and concluded on October 14th.

The results of this initial drill program at Tinkas are encouraging and indicate there is the potential for incremental resource extension. The best intersections include 11m at 1,273 ppm (TUBR1180), 11m at 777 ppm (TUBR1179), 14m at 311 ppm (TUBR1225) and 10m at 263 ppm (TUBR1174).

These discoveries highlight that tributaries of the main Tumas paleochannel, like at the S-Bend and Tinkas are prospective for future resource delineation that may add incremental value to the Tumas Project by potentially extending the LOM (Life of Mine) beyond the current 30-year resource base.

UPDATE ON THE URANIUM INDUSTRY

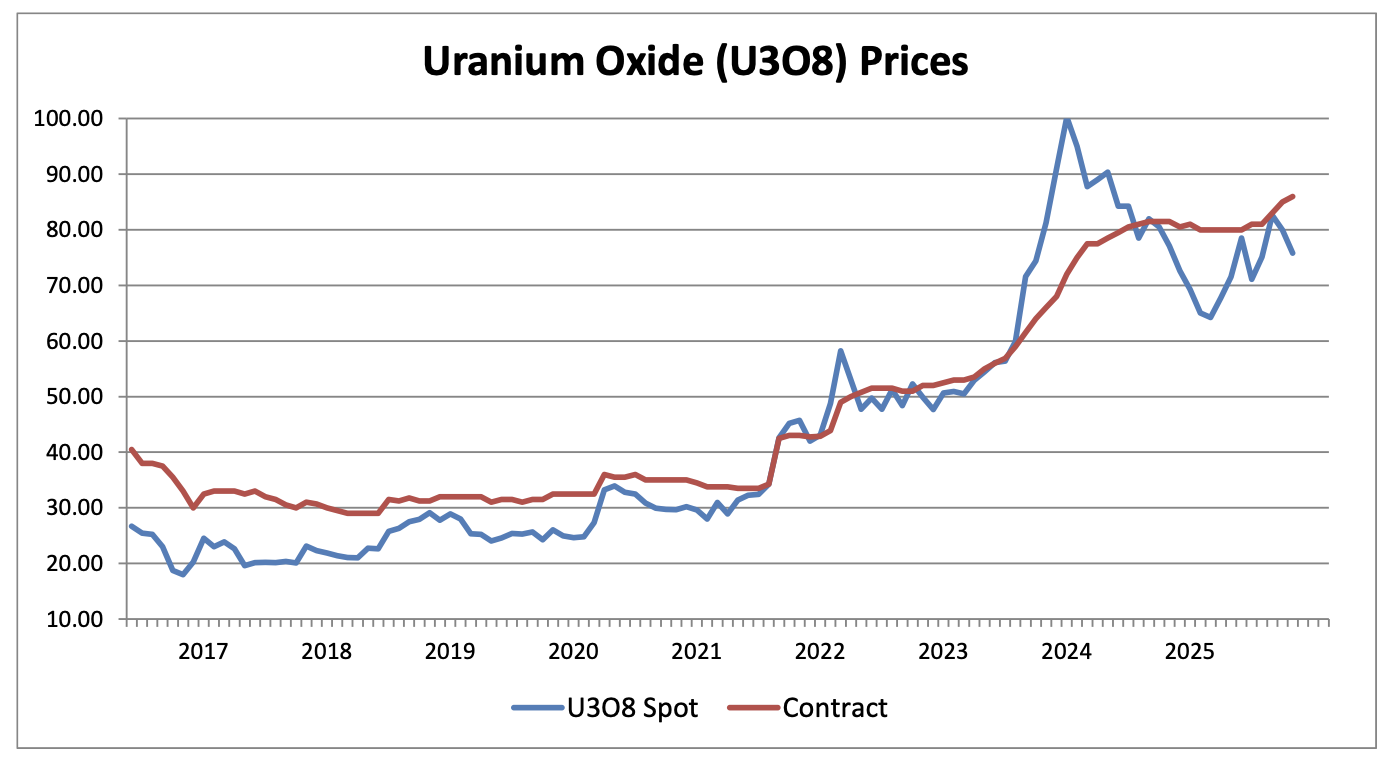

The spot price of U3O8rallied 18.3% from $63.50 per lb. U3O8 in mid-March to $75.80 per lb. in November while the long-term contract price has risen 7.5% to US$86.00 per/lb. from $80.

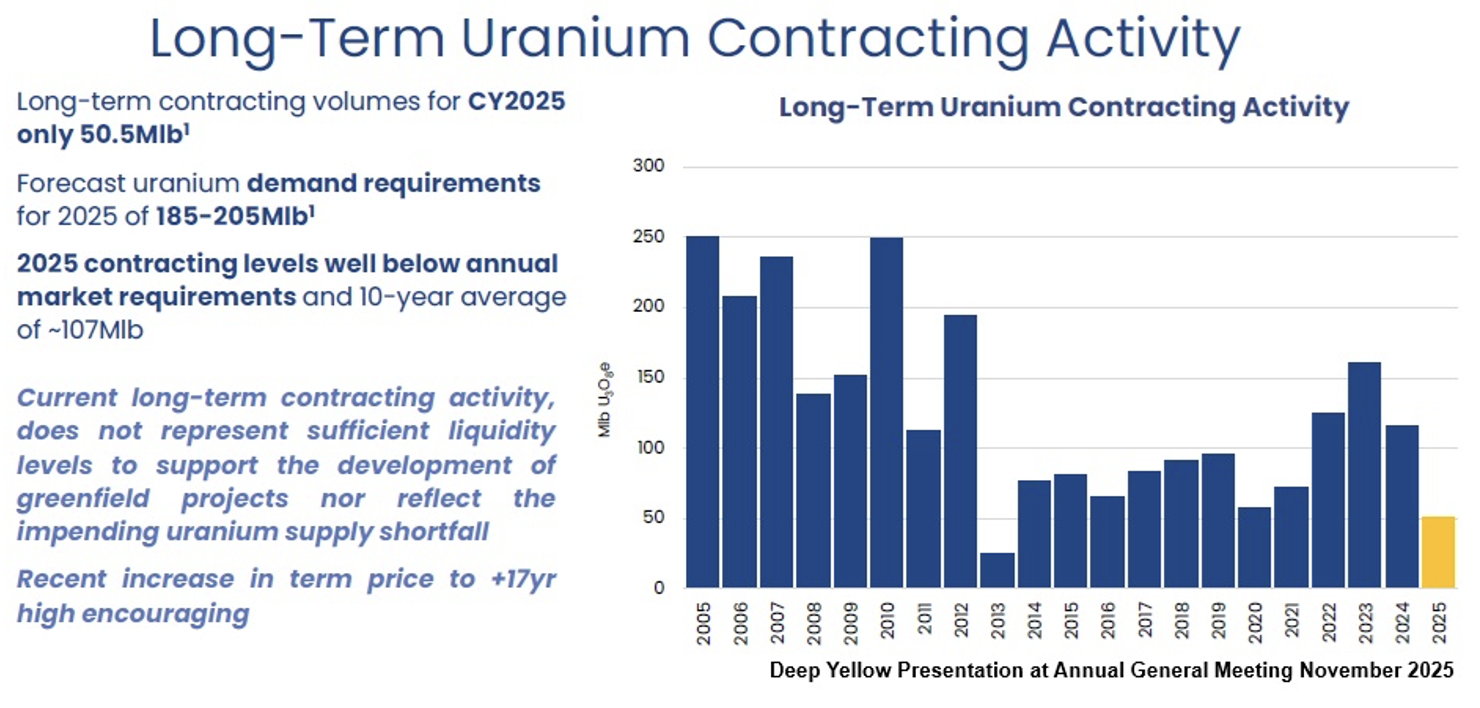

Through November 2025, volume has been very low with only 50 Mlbs having been contracted in the long-term market, well below (over 70% below) the level of replacement (185-205 Mlbs), which reflects delays in procurement due to buyer indecision and by price volatility. At some point, utility buyers will act on the realization that the structural supply deficit is deepening as major producing mines are entering the end of their production cycles coupled with declines in secondary supply.

The demand for uranium is poised to rise driven by expanding nuclear programs, such as reactor restarts, life extensions, new builds, the build-out of energy-hungry data centers and the emergence of SMR units. Without little macroeconomic and substitution risk, uranium remains a commodity with truly inelastic demand.

VALUATION

Broadly speaking, the public uranium companies can be grouped into three segments: producers, development companies and exploration companies. Producers are actively mining and generating revenues. Exploration companies are prospecting and/or drilling to establish mineral resources. In between these two segments are the development companies that already have established resources and are advancing through the process to bring a mine in operation, generally from the point of initiating a Pre-Feasibility Study to the actual construction of a mine. The comparable companies to Deep Yellow fall into this category.

Further, the comparable companies have been narrowed through quantitative factors, particularly those with a market capitalization over $700 million and trading above $1.00 per share. This process captures a range of well-funded junior uranium development companies, which are listed in the table above. Currently, the P/B valuation of these comparable companies is depressed in the 2.97-to-8.97 range. With the expectation that Deep Yellow’s stock can attain a P/B ratio of 4.8, our valuation price target is US$2.14.

SUBSCRIBE TO ZACKS SMALL CAP RESEARCH to receive our articles and reports emailed directly to you each morning. Please visit our website for additional information on Zacks SCR.

DISCLOSURE: Zacks SCR has received compensation from the issuer directly, from an investment manager, or from an investor relations consulting firm, engaged by the issuer, for providing research coverage for a period of no less than one year. Research articles, as seen here, are part of the service Zacks SCR provides and Zacks SCR receives payments totaling a maximum fee of up to $50,000 annually for these services provided to or regarding the issuer. Full Disclaimer HERE.