By John Vandermosten, CFA

NASDAQ:GRCE

READ THE FULL GRCE RESEARCH REPORT

Grace Therapeutics, Inc (NASDAQ:GRCE) announced that it has submitted its GTx-104 new drug application (NDA) to the FDA. This is a meaningful milestone for the company and may release additional capital if the NDA is accepted. We expect the FDA to announce its acceptance in the August 2025 timeframe. The submission announcement follows the report of fiscal year 2025 financial results and the filing of Grace’s Form 10-K. As a reminder, in February the company announced results for the Phase III STRIVE-ON trial. The most significant results came from the Phase III safety trial. In patients, it found excellent relative dose intensity, better outcomes, fewer intensive care unit readmissions and fewer ventilator days for GTx-104 compared with oral nimodipine.

In its earnings release, Grace highlighted its recent achievements including the pre-NDA meeting with the FDA, its target of submitting the NDA during 1H:25 (which was confirmed two days later) and the raise of additional capital that offers warrants that can be called if certain milestones are met. CEO Prashant Kohli communicated the STRIVE-ON trial data asserting that the information is supportive of improved clinical outcomes in aneurysmal subarachnoid hemorrhage (aSAH). Management’s focus will now shift towards commercialization efforts for GTx-104 in the upcoming months.

Fiscal Year 2025 Financial and Operational Results

Grace reported fiscal year 2025 results in a press release and a Form 10-K filing with the SEC on June 23rd. For the twelve-month period ending March 31st, 2025, operating expenses of $16.7 million were recognized. Net loss for 2025 totaled ($9.6) million or ($0.79) per share. After adjusting for other items, net loss was ($12.8) million or ($1.06) per share. Fiscal year 2025 compared to the prior year:

- General & Administrative expenses were $7.2 million, up 11% from $6.4 million attributable to higher legal, tax, accounting and other professional fees related to the change of jurisdiction of incorporation from Canada to the US. Other factors contributing to the increase were salaries, benefits and a headcount increase. These were partially offset by lower taxes and miscellaneous expenses;

- Research and development expenses rose 103% to $9.5 million from $4.7 million as a result of increased research activities for the GTx-104 program;

- Net interest and other income were $3.9 million compared to ($348,000) with the difference predominantly related to a change in fair value of derivative warrant liabilities related to an increase in Grace stock price. Interest income fell due to lower average cash balances;

- Net loss was ($9.6) million vs. ($12.8) million or ($0.79) per share vs ($1.35). After removing amounts related to change in fair value of derivatives and foreign exchange loss, net loss was ($12.8) million or ($1.06) per share.

As of March 31st, 2025, cash and equivalents carried on the balance sheet totaled $22.1 million. This amount compares to the $23.0 million cash balance held at the end of 2023. Net cash from financing for fiscal year 2025 was $14.0 million generating net proceeds of approximately $13.8 million.

New Drug Application (NDA) Submission

As expected, Grace Therapeutics submitted its new drug application (NDA) to the FDA before the end of the second quarter. Following the pre-NDA meeting held with the FDA earlier in the year, management felt closely aligned with the agency in terms of NDA acceptance requirements. It spent the next several months preparing the related documents and on June 24th announced that it had submitted its application.

Grace is in a strong financial position with approximately $22 million in cash as of March 31st, 2025 and a product that meets a profound unmet need. During previous equity capital raises, Grace was able to structure these deals so that the attached warrants could be called upon after achieving certain milestones. The company will be able to demand exercise of warrants that can potentially generate about $7.6 million following NDA acceptance and about $15 million following approval of GTx-104 assuming the warrants are in the money. Following normal regulatory timelines, we could see the first milestone met in the August timeframe if the FDA accepts the application.

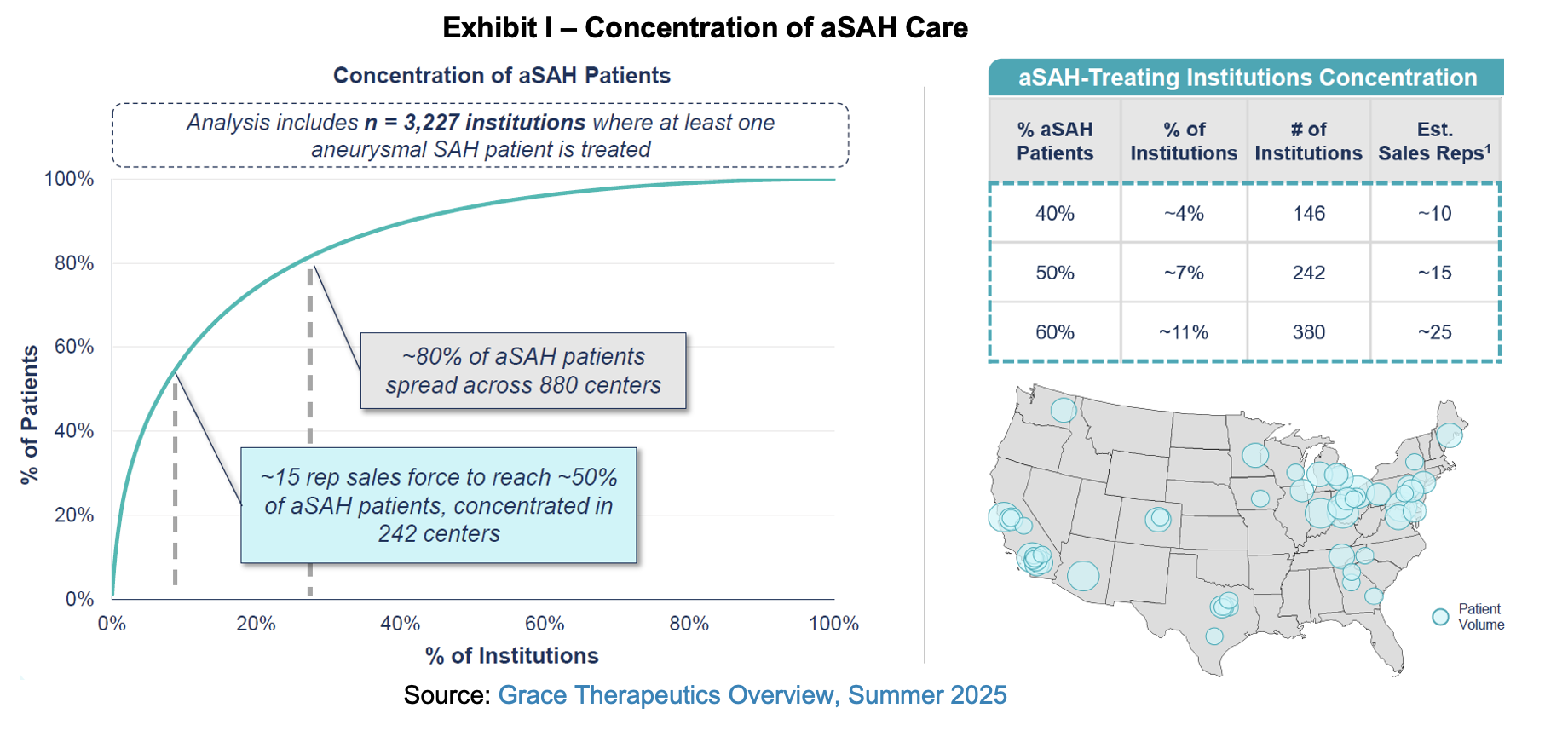

With the funds on the balance sheet and additional capital raised from the warrant exercises, Grace will be able to begin commercialization activities. Its plan is to focus on the top 250 to 300 hospitals that address aneurysmal subarachnoid hemorrhage (aSAH), which is achievable with a sales force of 15 to 20. We expect to hear more about the strategy in the coming months and following the conclusion of marketing studies the company is conducting.

Investment Thesis

Grace’s GTx-104 investment thesis is straightforward. There are about 40,000 aSAH cases per year in the United States that in many cases are inadequately served. Oral nimodipine is standard of care. The underlying drug has demonstrated its efficacy in increasing blood flow to the brain, reducing brain damage and improving neurological outcomes. However, nimodipine is only available in oral form which presents several shortcomings. The primary weakness is that the oral formulation is difficult to administer to patients that are unconscious or have a hard time swallowing, which is a common feature of aSAH patients. Oral nimodipine should be administered every four hours due to its short half-life and it should not be taken with food as this further reduces its already low bioavailability. Oral nimodipine has low and inconsistent bioavailability due to first-pass metabolism and poor solubility, resulting in reduced systemic exposure. Higher blood plasma levels can cause hypotension which is associated with neurological impairment, organ damage, reduced kidney function and other risks. Europe offers an IV formulation of nimodipine branded Nimotop; however, the product solubilizes the drug with high levels of ethanol and propylene glycol. These excipients have numerous negative effects and prevented FDA approval of Nimotop. Grace’s IV formulation uses excipients generally recognized as safe (GRAS), and provides a product which is able to improve upon the ethanol-based European version and the oral formulation’s primary weaknesses.

Results from Grace’s Phase III safety trial found excellent relative dose intensity, better outcomes, fewer intensive care unit readmissions and fewer ventilator days for GTx-104 compared with oral nimodipine. The trial met its primary endpoint of the number of patients with at least one episode of clinically significant hypotension reasonably considered to be caused by the drug. Patients receiving GTx-104 experienced a 19% reduction in at least one incidence of clinically significant hypotension compared to oral nimodipine (28% versus 35%). Secondary endpoints include safety, clinical and pharmacoeconomic outcomes. Additional detail on the trial can be found in Grace’s press release and in our report.

We assign Grace a $12.50 valuation which provides upside of over 4x. It is a relatively lower risk development play as the underlying drug is already approved, the new formulation addresses significant unmet needs and all of the development work is complete, generating compelling results. While the company plans to develop GTx-104 itself, we think that additional value could be recognized if an established pharmaceutical company buys the asset and folds it into its operations.

In support of the reiteration of the thesis for the company, we recorded a short clip highlighting reasons to own Grace Therapeutics.

Milestones

- Pre-NDA meeting with FDA – 2Q:25

- NDA submission to FDA – June 2025

- $7.6 million warrant exercise if NDA accepted & above $3.00 strike – Fall 2025

- Target Action Date – mid-2026

- $15 million warrant exercise if GTx-104 approved & above $3.39 – Fall 2026

- GTx-104 commercialization – late 2026

SUBSCRIBE TO ZACKS SMALL CAP RESEARCH to receive our articles and reports emailed directly to you each morning. Please visit our website for additional information on Zacks SCR.

DISCLOSURE: Zacks SCR has received compensation from the issuer directly, from an investment manager, or from an investor relations consulting firm, engaged by the issuer, for providing research coverage for a period of no less than one year. Research articles, as seen here, are part of the service Zacks SCR provides and Zacks SCR receives quarterly payments totaling a maximum fee of up to $40,000 annually for these services provided to or regarding the issuer. Full Disclaimer HERE.