By Ronald Wortel, MBA, P. Eng.

OTC:LFLRF

READ THE FULL LFLRF RESEARCH REPORT

LaFleur Minerals (OTC:LFLRF) has entered 2026 with a decisive shift in its investment profile. The Company’s recently published Preliminary Economic Assessment (PEA) confirms that its Swanson gold deposit, paired with the fully permitted Beacon Gold Mill, can support a profitable, near‑term production scenario in Quebec’s Tier‑1 Abitibi gold belt. For investors, the combination of a validated mine plan, a permitted processing facility, and a strengthening gold market creates a compelling setup for value realization over the next 12–24 months.

The PEA outlines a modest‑capex, low-risk restart strategy anchored by C$31 million in initial capital and an after‑tax NPV5% of C$101 million at a base‑case gold price of US$2,750 per ounce. At current prices, the project’s leverage becomes more pronounced: sensitivity analysis shows NPV rising toward C$270 million at US$5,000 gold, a roughly 170% increase for an 80% move in the commodity.

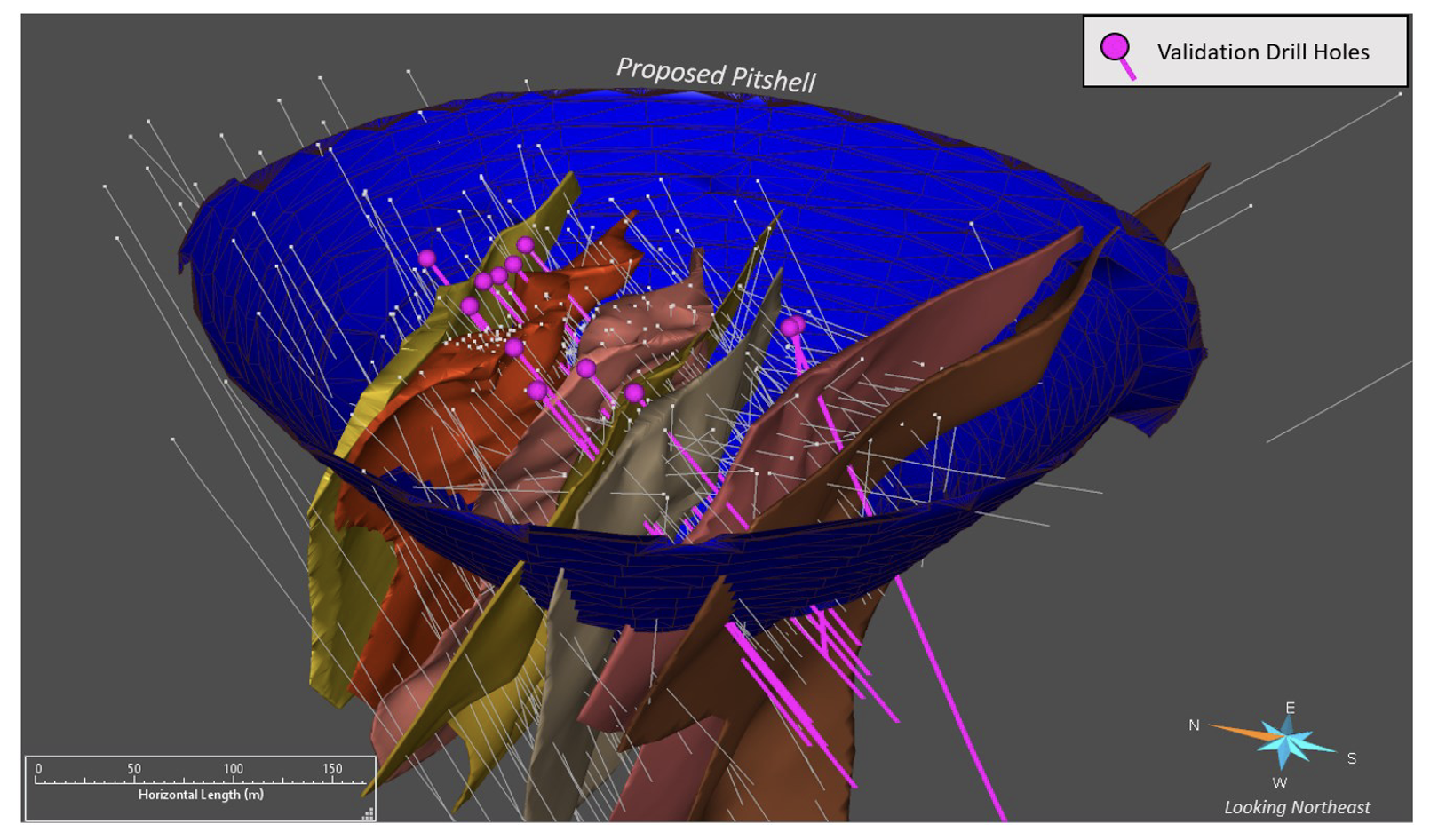

The updated mineral resource estimate provides further support for the development plan. Indicated ounces increased by 30% following confirmation drilling and lower cut‑off grades, bringing the total to 160,000 ounces indicated and 67,000 ounces inferred. Importantly, most of the indicated resource sits within the optimized pit shell, supporting several years of low-cost open-pit mining before transitioning to underground potential. The mineralized footprint—475 metres by 425 metres by 500 metres—remains open in all directions, and ongoing drilling continues to demonstrate extensions at depth, on strike, and internally within the deposit.

Operational readiness is another differentiator. The Beacon Gold Mill is fully permitted, refurbished, and funded for restart following a C$7 million financing. Tailings capacity exceeds 10 years at nameplate throughput, and a 10,000-tonne stockpile of mineralized material on site provides a low-risk commissioning feed. Metallurgical testing underway at SGS Canada is expected to refine recovery assumptions and potentially improve upon the 84% recovery rate used in the PEA.

Investors should remain aware of several risks. Permitting for the 100,000-tonne bulk sample at Swanson remains outstanding, with approval expected later in 2026. The mill restart requires final technical validation, and capital markets volatility could affect funding for the larger 1,250‑tpd expansion scenario. As with all junior miners, gold price sensitivity remains a central factor in valuation and project timing.

Despite these risks, LaFleur’s strategic positioning is notable. The company controls a district-scale land package with 27 mineral showings and sits adjacent to Fresnillo’s newly acquired Novador project, creating potential for regional consolidation. The valuation gap is also significant: at a market capitalization of roughly C$38 million, LaFleur trades at a steep discount to its PEA-derived NAV and well below peer P/NAV multiples.

Taken together, LaFleur Minerals offers investors a rare combination of a permitted mill, a growing resource base, and a validated economic plan, all in a Tier‑1 jurisdiction. With multiple catalysts ahead, including ongoing drill results, bulk sample approval, and mill commissioning, the Company is positioned for a meaningful re-rating as it advances toward production.

SUBSCRIBE TO ZACKS SMALL CAP RESEARCH to receive our articles and reports emailed directly to you each morning. Please visit our website for additional information on Zacks SCR.

DISCLOSURE: Zacks SCR has received compensation from the issuer directly, from an investment manager, or from an investor relations consulting firm, engaged by the issuer, for providing research coverage for a period of no less than one year. Research articles, as seen here, are part of the service Zacks SCR provides and Zacks SCR receives payments totaling a maximum fee of up to $50,000 annually for these services provided to or regarding the issuer. Full Disclaimer HERE.