By John Vandermosten, CFA

NASDAQ:LGND

READ THE FULL LGND RESEARCH REPORT

Ligand Pharmaceuticals, Inc. (NASDAQ:LGND) reported 2025 results with revenues of $268 million and adjusted core earnings per share (EPS) of $8.13. Both numbers were substantially better than initial and revised 2025 guidance. Isolating the fourth quarter results, revenues from royalties were markedly better than our estimates, while Captisol revenue was slightly below and the highly volatile Contract Revenue was below our estimates due to timing. In the fourth quarter, royalties grew 45% and Captisol fell 1.5%. Contract Revenue was $1.3 million in the fourth quarter compared with $89,000 in the same prior year period. Other activity since the December analyst day includes a number of partner clinical and regulatory achievements and a refinement in the portfolio management strategy that seeks to optimize the relationship Ligand has with its partners. A few recent material highlights include Palvella Therapeutics’ QTORIN data, a delay in the target action date for Filspari by three months and the resurrection of lasofoxifene. Along with its earnings release, Ligand reiterated 2026 guidance of revenues between $245 and $285 million and earnings per share of $8.00 to $9.00.

2025 Financial and Operational Results

Ligand reported 2025 financial and operational results in a press release and Form 10-K filing with the SEC on February 26th and 27th, respectively. A conference call was held with an accompanying presentation to discuss results with investors following the release. For the year ending December 31st, 2025, Ligand recognized revenues of $268.1 million. GAAP earnings per share for 2025 totaled $6.13, and core adjusted EPS was $8.13. For 2025 versus the same prior year period:

- Revenues of $268.1 million rose 60% from $167.1 million, amplified by a significant contribution related to the spin out of Pelthos. Royalty revenues increased by 48%, driven by contributions from Travere Therapeutics’ Filspari as well as Merck’s Capvaxive and Ohtuvayre. Captisol revenues rose 30% to $40.2 million due to the timing of customer orders. Contract revenue and other income increased 143% to $66.9 million and includes $53.1 million related to the Pelthos transaction;

- Cost of revenue, which is related to Captisol cost of goods sold, totaled $14.5 million, increasing 31% over prior year levels. The increase is due to higher Captisol sales, partially offset by lower gross margin, which fell by 30 basis points to 63.8%;

- Amortization of intangibles was $32.7 million vs. $33.0 million, with the change due to deconsolidation of LNHC, the holding vehicle for the spin-out of Pelthos, on July 1st, 2025;

- Research and development expense totaled $81.2 million versus $21.4 million, with $17.8 million of the amount attributable to the acquisition of the AVIM Therapy royalty rights from Orchestra;

- General & Administrative expenses were $92.4 million, up 18% from $78.7 million, with the increase primarily due to transactions costs;

- Financial royalty impairment was $6.2 million, related to UGN-301 and other Agenus partner programs, compared with $30.6 million related to the soticlestat program;

- Total non-operating items were $118.0 million vs. $25.1 million. Material items include a $90.7 million gain related to the Pelthos transaction, an $18.4 million gain from short-term investments, $13.7 million in interest income offset by $4.7 million of interest expense related to the convertible bond issued in August 2025, and other minor non-operating expenses;

- Income tax expense of $34.5 million represents a tax rate of 21.7%;

- Net income was $124.4 million ($6.13 per share) versus a net loss of $4.0 million (-$0.22 per share). Adjustments to 2025 GAAP earnings added $2.00 per share to generate core earnings of $8.13 per share.[1]

As of December 31st, 2025, cash, equivalents, and short-term investments totaled $734 million. This amount compares to the $256 million balance held at the end of 2024. Free cash flow for the year totaled $48.9 million, while cash from financing was $428 million, largely due to proceeds from the convertible note issuance. The company maintains access to a revolving line of credit and an at-the-market (ATM) facility with Stifel, Nicolaus, that can expand its access to capital as needed.

Portfolio Management Process

During its fourth quarter call, management announced a new portfolio management process that seeks to improve the opportunities presented by the existing portfolio of over 100 therapeutic assets. Ligand believes that there are new indications, markets, and prospects for its portfolio constituents and plans to increase communication with its royalty and investment partners to identify these possibilities. Key objectives of the initiative include:

- Ensuring partners have the information and capital they need to successfully optimize their assets;

- Offering capital and expertise to attractive programs;

- Broadening existing collaborations.

Ligand will accomplish this task by identifying novel ways to expand the partnership. This includes efforts to be more proactive, data driven, and investment focused across the portfolio.

Palvella Therapeutics

Ligand holds both an equity stake in Palvella Therapeutics and a royalty interest in its QTORIN platform. The relationship began in December 2018 when Ligand entered into a development funding and royalties agreement with Palvella covering PTX‑022 (QTORIN 3.9% rapamycin gel) and at least one additional program (e.g., PTX‑367), contributing $10 million to Palvella up front in exchange for tiered royalties in the mid‑to‑upper single digits on net sales plus regulatory and financing milestones. In late 2023, Palvella and Ligand announced an expanded strategic partnership to accelerate Phase III development of QTORIN rapamycin for microcystic lymphatic malformations (MLMs). This increased the tiered royalty on commercial sales of the drug to 8.0 - 9.8%. Ligand also secured an option to obtain a single-digit royalty on each future topical product derivative from the QTORIN platform.

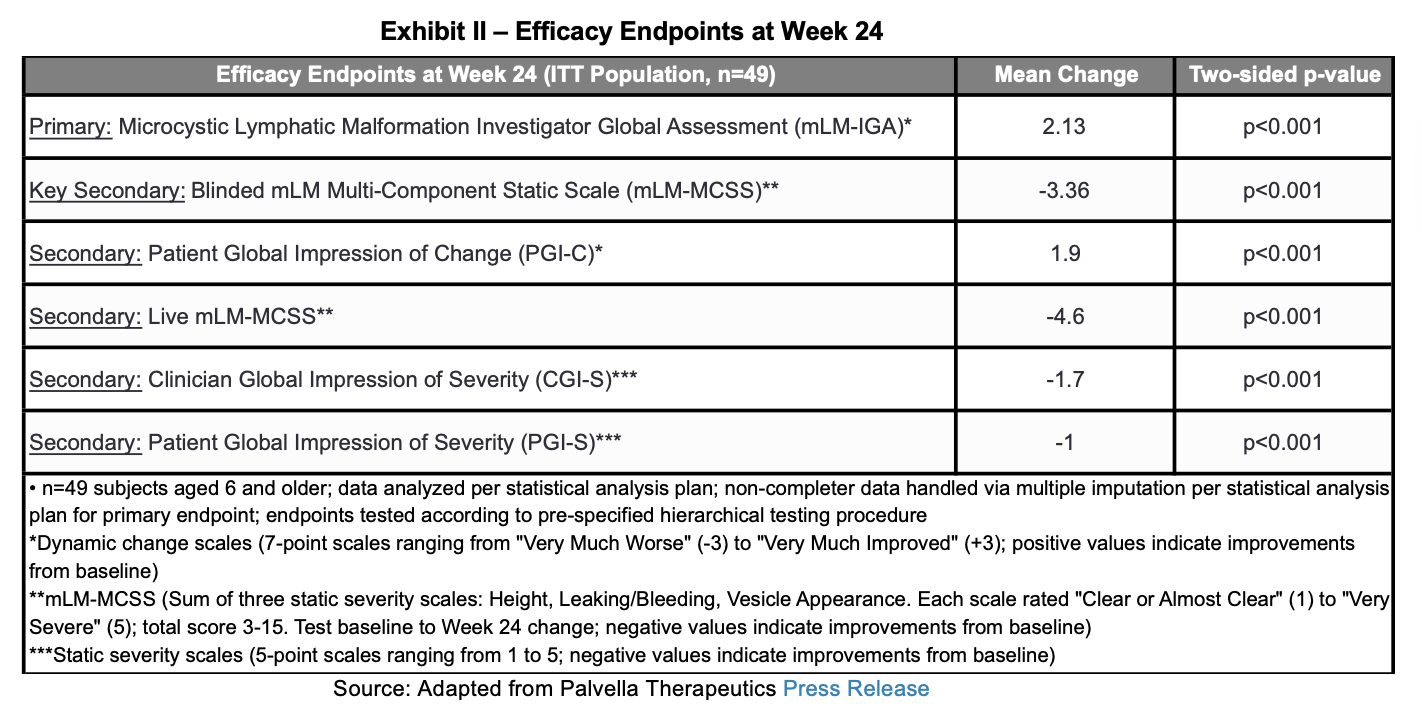

In January, Palvella provided an update on its portfolio, noting that its Phase III SELVA study is on track for a March 2026 report of topline data. On February 24th, 2026, Palvella announced topline results from the clinical study evaluating QTORIN in MLMs. Along with the press release, Palvella held a conference call to discuss results and published a slide deck providing additional details.

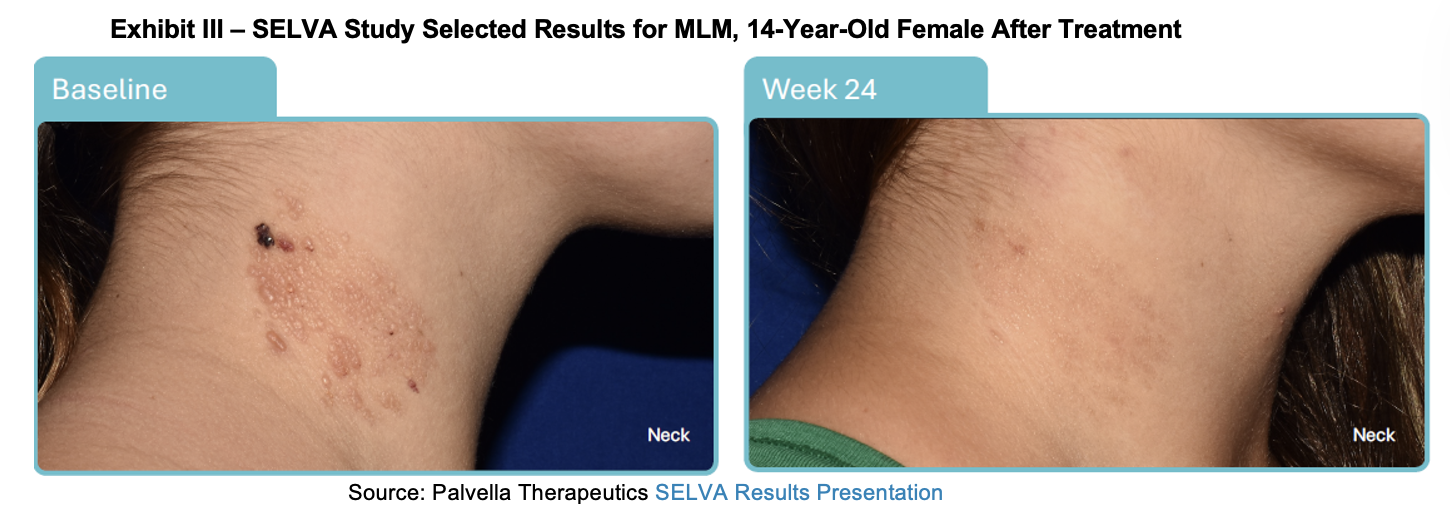

The study achieved its primary endpoint of a statistically significant improvement of 2.13 (p < 0.001) units on the Microcystic Lymphatic Malformation Investigator Global Assessment (MLM-IGA). Additionally, the study achieved statistical significance on the pre-specified key secondary endpoint of blinded MLM Multi-Component Static Scale (MLM-MCSS) and all four secondary efficacy endpoints. 95% of the subjects in the trial over the age of 6 who completed the efficacy evaluation improved on the MLM-IGA at week 24. Below we summarize the efficacy endpoints.

Similar to previous clinical trials, the SELVA study generated data showing that QTORIN was well-tolerated. Among the 50 participants who initiated treatment, 35 participants (70%) experienced treatment-emergent adverse events (TEAEs). Four experienced serious adverse events, of which one experienced a severe TEAE. All TEAEs were deemed unrelated to the study drug by investigators. Among the TEAEs, a total of 17 participants experienced treatment-related adverse events (TRAEs), all of which were rated mild or moderate. The most common TRAEs included application site acne, application site discoloration, and application site pruritus (n=3, 6%). Rapamycin levels were below 2 ng/mL in systemic circulation for all participants at all timepoints in the study.

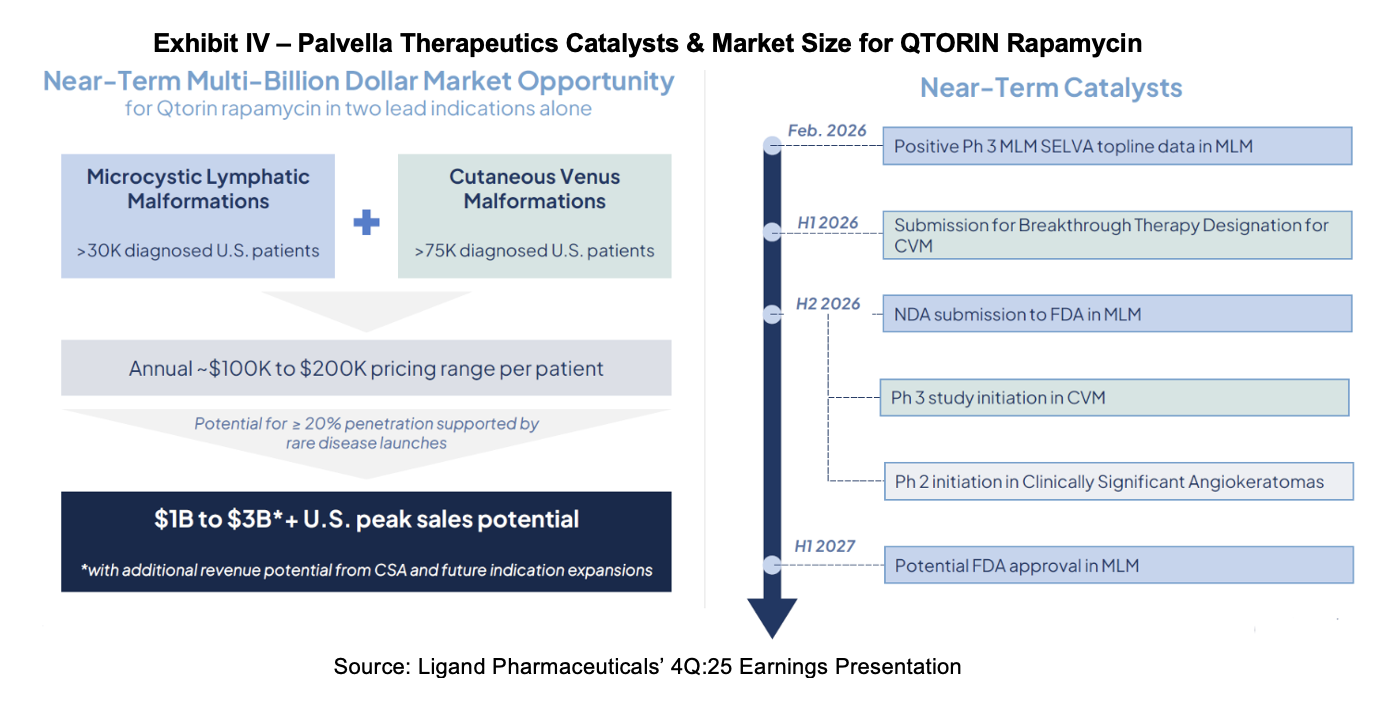

Palvella will develop a new drug application (NDA) to submit to the FDA for QTORIN rapamycin in 2H:26. Management anticipates that approval will be granted in 1H:27, taking advantage of Fast Track and Breakthrough Therapy designations.

Of the 50 participants who initiated treatment, 44 (88%) completed the 24-week efficacy evaluation period. Four participants discontinued for reasons unrelated to adverse events, one participant discontinued due to an adverse event not related to study drug, and one participant discontinued due to an adverse event (lymphorrhea) possibly related to study drug. Following completion of the efficacy evaluation period, 43 of 44 eligible participants elected to continue treatment during the extension period.

QTORIN Rapamycin

QTORIN rapamycin is a topical mTOR (mechanistic/mammalian target of rapamycin) inhibitor for rare, serious dermatologic conditions like pachyonychia congenita and microcystic lymphatic malformations. It is designed to selectively inhibit overactive mTOR signaling in skin lesions, particularly in conditions driven by PI3K–AKT–mTOR pathway dysregulation. By locally inhibiting mTOR, the drug aims to reduce endothelial cell hyper‑proliferation and abnormal vascular/lymphatic signaling (e.g., VEGF), thereby shrinking or stabilizing vascular and lymphatic malformations.

Phase II results for QTORIN were announced in December 2025 for clinically significant angiokeratomas. On December 16th, Palvella announced that the FDA had granted Fast Track for the drug in this indication. The grant of this expedited treatment opens the drug up to Accelerated Approval and Priority Review in the future. Palvella anticipates starting a Phase II trial for the product in 2H:26. Angiokeratomas are small, firm bumps on the skin that typically appear dark red, purple, or even black. They are benign skin lesions consisting of an angioma (a cluster of dilated surface blood vessels) covered by a keratoma (a thickened layer of skin). They are treated using laser therapy, cryotherapy, or electrocauterization. Ligand cites 50,000 diagnosed cases of angiokeratomas per year in the United States.

QTORIN is also in development for cutaneous venous malformations (CVMs). It was recently the subject of a Phase II trial readout in December 2025, where most patients in the trial demonstrated improvement. A Phase III trial is planned. CVM is a rare genetic disease caused by mutations that overactivate the PI3K/mTOR signaling pathway, leading to dysfunctional veins in the skin. There are no FDA-approved therapies for patients suffering from the disease. Treatment is focused on addressing symptoms and can include sclerotherapy, laser therapy, compression garments, and surgical resection.

Palvella’s QTORIN appears to be in a strong position and is on the cusp of submission to the FDA for approval in MLM with a favorable safety and efficacy profile. The asset has two other indications in angiokeratomas and CVMs, which will also generate royalty revenue for Ligand if they are ultimately approved and produce sales.

SUBSCRIBE TO ZACKS SMALL CAP RESEARCH to receive our articles and reports emailed directly to you each morning. Please visit our website for additional information on Zacks SCR.

DISCLOSURE: Zacks SCR has received compensation from the issuer directly, from an investment manager, or from an investor relations consulting firm, engaged by the issuer, for providing research coverage for a period of no less than one year. Research articles, as seen here, are part of the service Zacks SCR provides and Zacks SCR receives payments totaling a maximum fee of up to $50,000 annually for these services provided to or regarding the issuer. Full Disclaimer HERE.

________________________

[1] Details of the GAAP to core earnings reconciliation are in Ligand’s earnings press release. Material adjustments include Share-based compensation expense, Amortization, change in fair value for Pelthos securities and gain on sale of Pelthos.