By Thomas Kerr, CFA

NASDAQ: PMAX

OVERVIEW

Powell Max (NASDAQ: PMAX) is a holding company incorporated in the British Virgin Islands with primary operations in Hong Kong. Founded in 2019, the company went public in September 2024 and was listed on the NASDAQ at that time. The company’s key operating subsidiary is Hong Kong-based Jan Financial Press Limited, a provider of financial communications services that support capital market compliance and transaction needs for corporate clients and their advisors in the Hong Kong region (full description below).

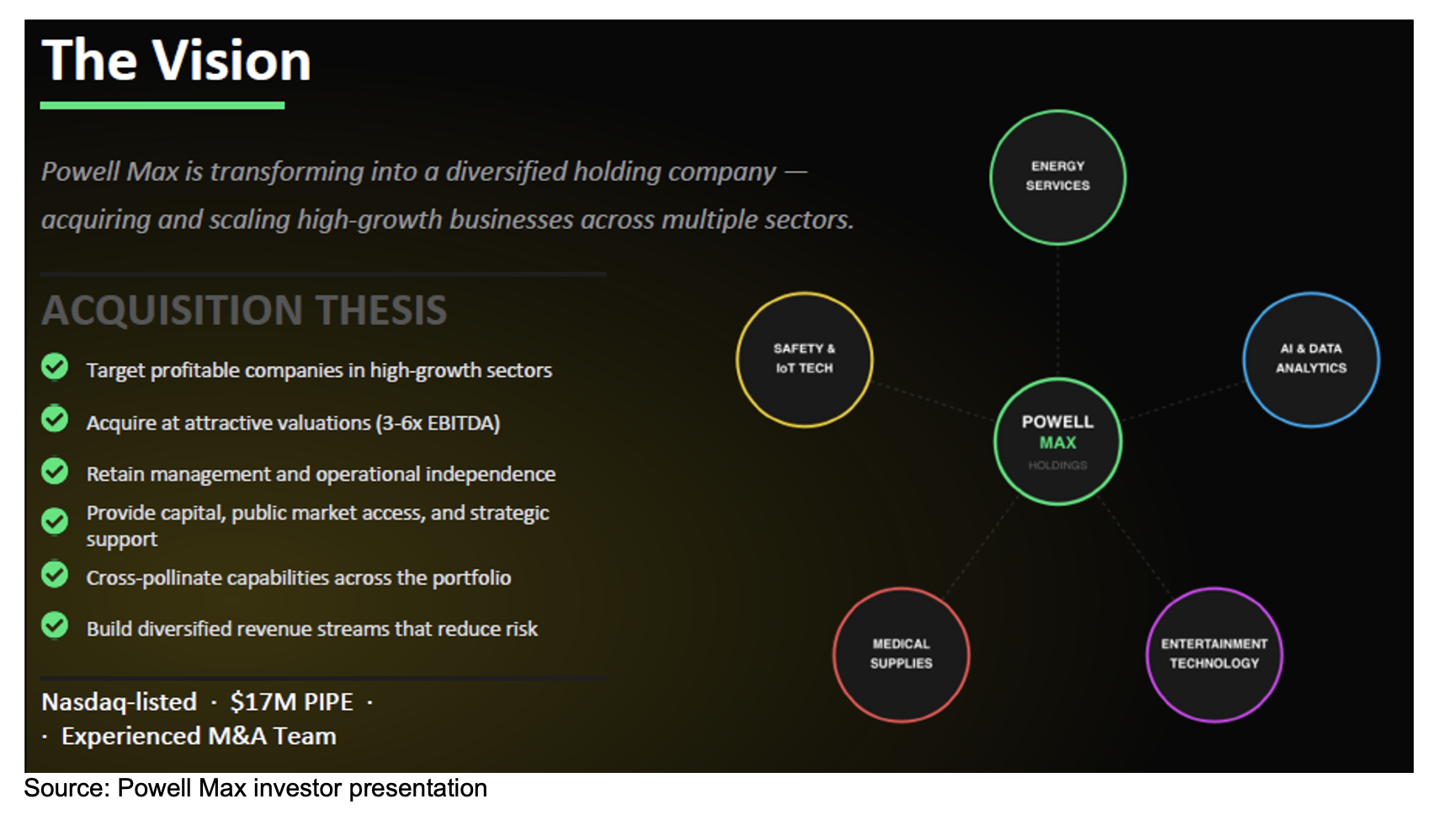

However, Powell Max has recently transformed into a broadly diversified holding company that will acquire and scale high-growth businesses across multiple industries and sectors. These acquisitions will be mostly U.S.-based and cover Energy Services, AI/Data Analytics, Entertainment Technology, Medical Supplies, and Safety & IoT Technology.

The company is led by a strong management team with extensive experience in mergers & acquisitions, corporate finance, capital markets, regulatory compliance, and scaling businesses across multiple sectors.

In January 2026, the company raised $17 million in funds through a PIPE transaction to pursue its acquisition strategy.

ACQUISITION CRITERIA

Powell Max’s acquisition strategy is focused on targeting profitable businesses operating in high-growth sectors and acquiring them at what management believes are attractive valuations. The goal is to acquire companies in the range of 3x-6x EBITDA. Following an acquisition, the company intends to retain existing management teams and preserve operational independence, while providing capital, public market access, and strategic support to help accelerate growth.

Over time, management aims to create additional value by leveraging synergies and driving collaboration across the portfolio and building diversified revenue streams, which should enhance resilience and reduce concentration risk at the broader platform level.

Management is targeting a scaled and diversified platform by 2027, with projected consolidated revenue of more than $50 million and a portfolio of over five companies within the next 18 months. The strategy focuses on increasing exposure to higher-quality recurring and SaaS revenue, which is targeted to exceed 40% of the overall mix. Collectively, the portfolio is also expected to include more than 30 patents, further supporting a long-term competitive moat.

PORTFOLIO OF COMPANIES

JAN FINANCIAL PRESS LIMITED

This is Powell Max’s current operating subsidiary. Founded in 2019 and based in Hong Kong, Jan Financial provides financial communications services to corporate clients and their advisors in Hong Kong, supporting capital markets compliance, regulatory reporting, and transaction execution. Its service offering covers the full financial reporting workflow, including financial printing, corporate reporting, translation, proofreading, typesetting, design, printing, electronic reporting, newspaper placement, and distribution.

The company helps clients meet disclosure and filing requirements while managing the accurate and timely preparation, production, and delivery of financial communications throughout the transaction lifecycle. Its client base includes domestic and international companies listed on the Hong Kong Stock Exchange, companies preparing to list on an exchange, and related professional advisors operating in Hong Kong.

In addition to its core communications offering, the company also provides ancillary support services such as conference room rentals and web hosting to help facilitate clients’ compliance and transaction-related needs.

BOSTON SOLAR (Letter of Intent)

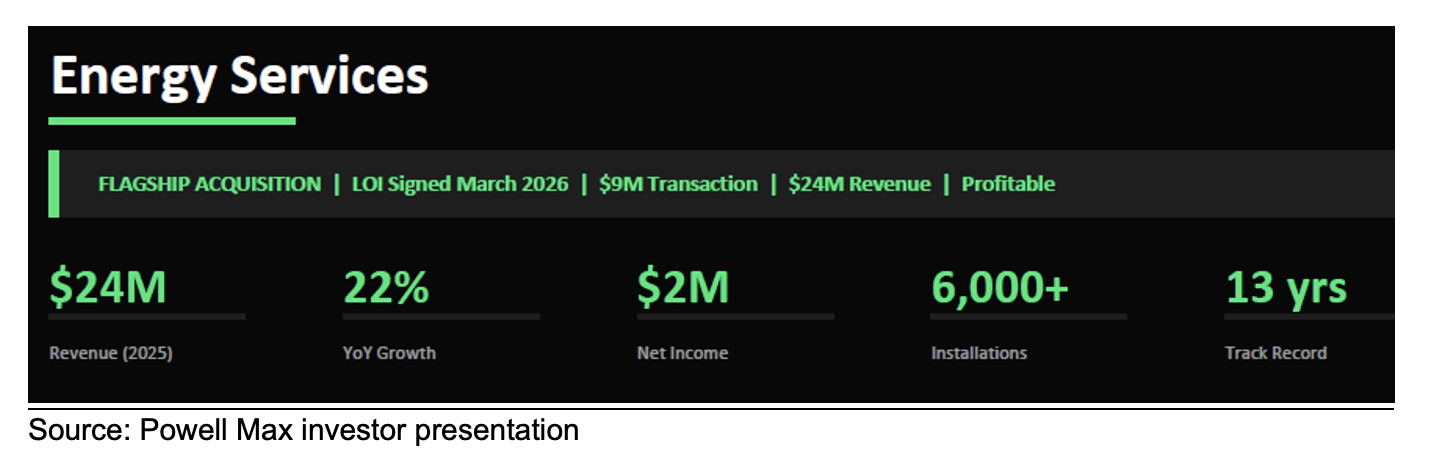

On March 23, 2026, Powell Max revealed its first acquisition by announcing it had signed a non-binding Letter of Intent to acquire The Boston Solar Company (“Boston Solar”), a vertically integrated regional engineering, procurement, and construction (EPC) solar installer operating in Massachusetts and the broader New England area.

The proposed transaction is valued at $9.0 million, including the assumption of up to $7.0 million in debt. Subject to normal due diligence, the parties expect to execute a definitive agreement no later than May 16, 2026. After closing, Powell Max expects to provide Boston Solar with up to $20 million in working capital funding to support operations and future growth.

According to Boston Solar, its revenue in 2025 increased by 22% to $24 million annual revenue and adjusted net income was approximately $2 million. The business was comprised of 65% residential and 35% commercial.

Boston Solar is vertically integrated to ensure the customer gets the most complete solar system for their needs. Boston Solar does it all, from financing to design and installation, with licensed and certified in-house installers.

The company has a successful 13-year track record and has its own strategic growth plans. This includes regional expansion beyond Massachusetts to five adjacent Northeast states, as well as service diversification into areas such as battery storage, EV charging, HVAC, and efficiency services. Under guidance from Powell Max, the company also has an M&A strategy in which it may make accretive acquisitions in New England, California, and Canada. The solar installation industry remains highly fragmented, with thousands of quality regional installers across the country operating without the capital or back-office support to scale.

Notable clients include Fenway Park (home of the Boston Red Sox), MGM Music Hall, a large federal agency, a luxury hotel chain, and various global manufacturers.

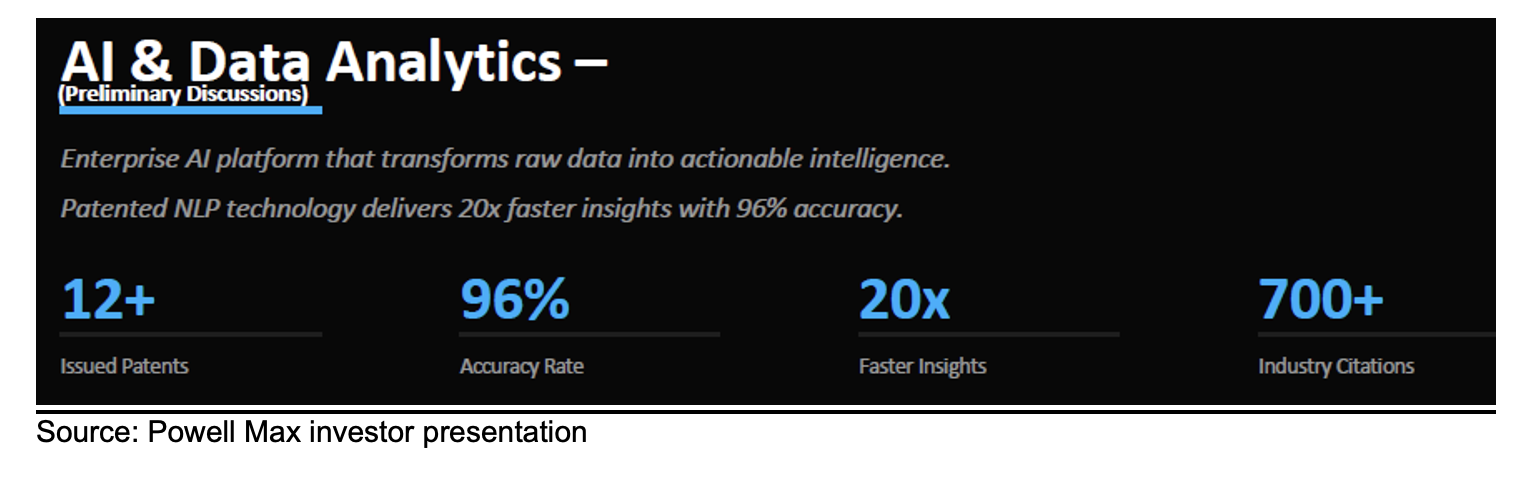

Unnamed AI & DATA ANALYTICS COMPANY (preliminary discussions)

Powell Max is in preliminary discussions to acquire an Enterprise AI platform that transforms raw data into actionable intelligence. It has patented Natural Language Processing (NLP) technology that delivers 20x faster insights with 96% accuracy.

The company to be acquired has core capabilities that are centered on converting complex information into actionable insight through advanced natural language processing, automated data harmonization across virtually any source, and a no-code platform that enables deployment by non-technical users. Its solutions are designed to support real-time model building and idea discovery, helping users accelerate research workflows, surface investment opportunities more efficiently, and improve decision-making across large, fragmented datasets.

The case for including this company in the Powell Max portfolio is supported by their differentiated intellectual property portfolio, which includes more than 12 patents and proprietary trade secrets that underpin a defensible competitive moat. Its technology has also been cited by major industry participants, including Apple, Microsoft, IBM, Google, and HPE, reinforcing the relevance and credibility of its platform. From a commercial perspective, the business operates under an enterprise SaaS model that offers recurring revenue potential, while its technology appears broadly applicable across PMAX’s portfolio companies, creating potential strategic value beyond a standalone acquisition. The opportunity is further supported by favorable industry tailwinds, with global AI spending projected to exceed $500 billion by 2030.

The size and financial data for this potential acquisition have not been disclosed at this time.

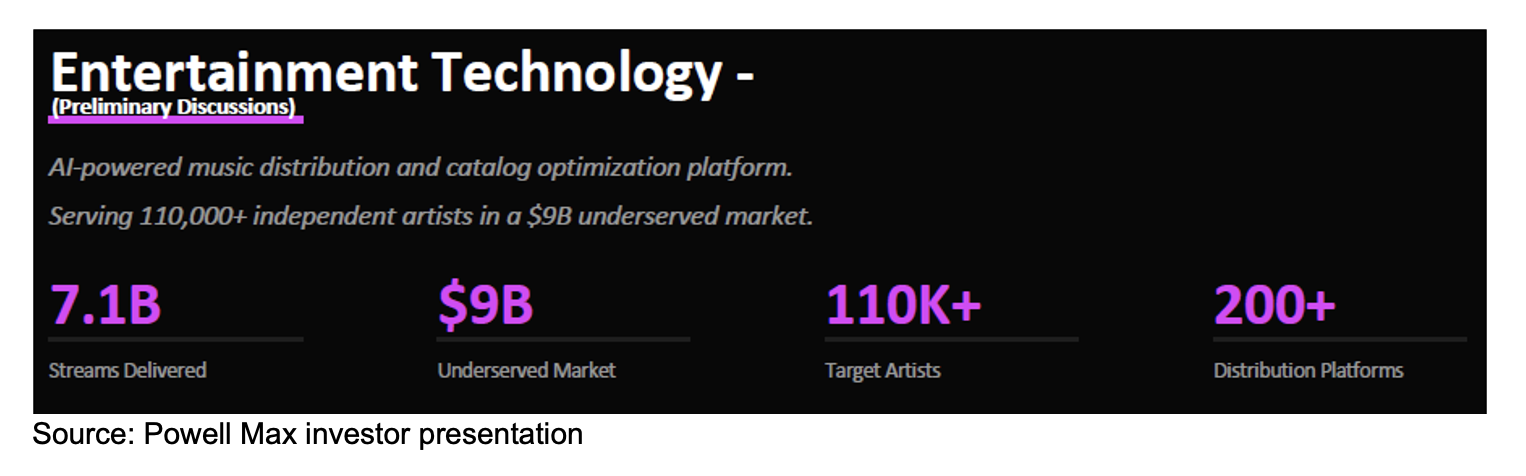

Unnamed Entertainment Technology (preliminary discussions)

Powell Max is in early conversations to acquire an AI-driven music distribution and catalog optimization platform that serves over 110,000 independent artists in a $9.0 billion underserved market.

The company’s recurring services offering is positioned to generate durable monthly recurring revenue through an AI-powered platform that supports global distribution across more than 200 platforms. The platform includes automated content creation and marketing, as well as predictive analytics designed to enhance artist performance and audience engagement. The platform also includes royalty optimization and recovery tools, which management indicates can drive more than 20% uplift, further strengthening the value proposition for creators and rights holders while supporting a scalable, high-margin recurring revenue model.

Another potentially high margin offering is the company’s catalog bundling strategy, which aggregates 20 to 50 music catalogs into diversified portfolios for sale to institutional buyers, typically at 8x-10x multiples. This model enables the company to generate transaction-based revenue through a 20% commission on each sale, while also retaining post-sale distribution rights that can provide an ongoing recurring revenue tail. This unique approach creates a capital-light monetization pathway that combines near-term fee generation with longer-duration recurring economics.

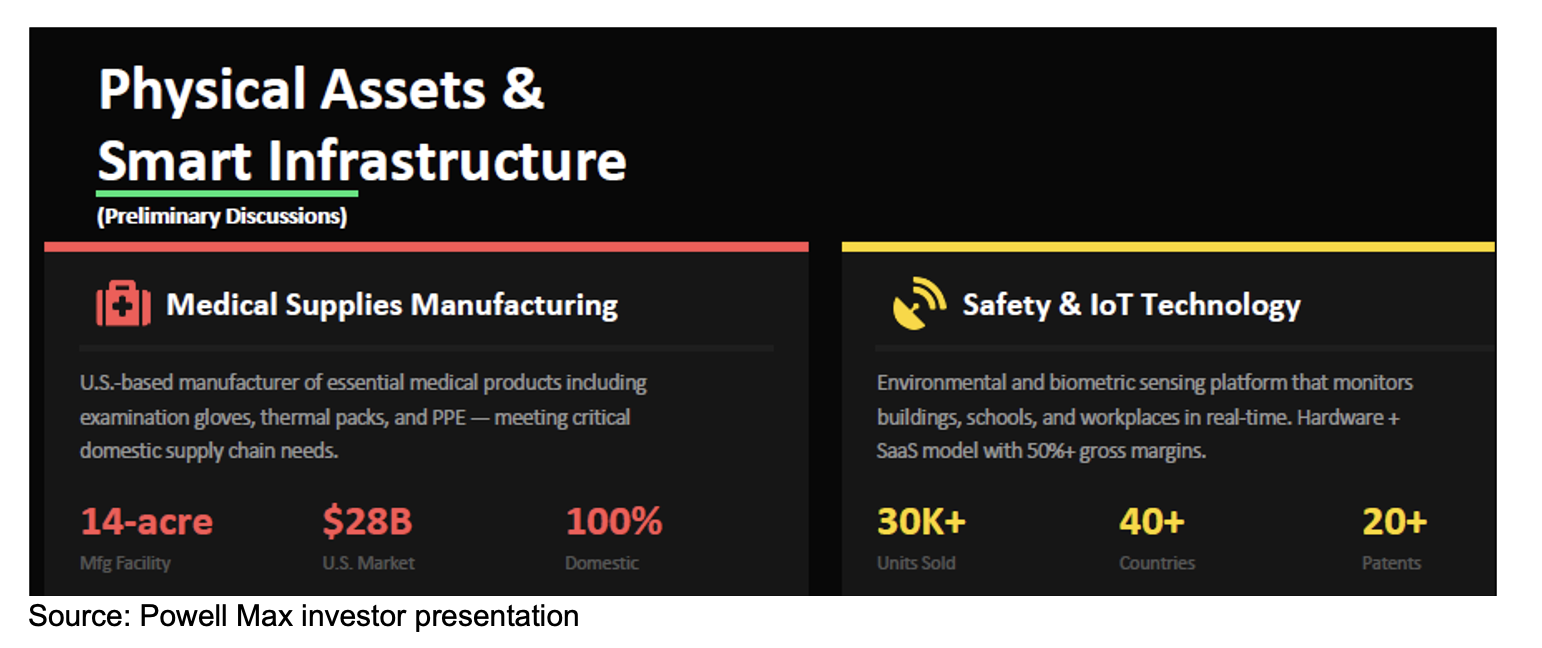

Unnamed Physical Assets & Smart Infrastructure (preliminary discussions)

Powell Max is in discussions to acquire a company with two distinct operating divisions:

Medical Supplies Manufacturing – This is a U.S.-based manufacturer of essential medical products, including examination gloves, thermal packs, and other personal protection equipment that meet critical domestic supply chain needs in the healthcare industry.

The company operates a vertically integrated business model, owning a 14-acre manufacturing facility that supports its broader mission of helping revitalize American manufacturing. The platform is positioned to benefit from sustained post-pandemic demand for PPE and workplace safety solutions, while also leveraging a rural workforce and cost structure that could provide operating advantages.

Safety & IoT Technology – This company has an environmental and biometric sensing platform that monitors buildings, schools, and workplaces in real-time. This hardware-plus-SaaS model reportedly generates gross margins in excess of 50% and has already achieved meaningful commercial traction, with more than 30,000 units sold across approximately 40 countries.

The business is currently focused primarily on the K-12 school market, with expansion into enterprise applications underway, and is supported by a growing global distribution footprint of more than 60 resellers. Its competitive positioning is further reinforced by a substantial intellectual property portfolio that includes more than 20 U.S. and international patents that creates a meaningful barrier to entry.

COMPETITIVE ADVANTAGE

By operating across diverse industries, the company is able to reduce portfolio risk while at the same time generating meaningful synergies across the portfolio.

Advantages of this portfolio and acquisition strategy include:

- AI-Enabled Platform Strategy – The company plans to deploy AI/NLP across its energy operations, medical QC, safety monitoring, and entertainment analytics divisions.

- Shared Infrastructure - The portfolio of Powell Max companies will utilize shared centralized finance, human resources, IT, legal, and compliance platforms in order to generate cost synergies.

- Capital Efficiency – Acquired companies will have public market access and access to equity facilities of the holding company to support growth and working capital objectives.

- Geographic Reach – Operations from the portfolio of companies span North America and over 40 other international countries.

- Revenue Diversification – There is no single-sector dependency, and the portfolio companies are diversified across hardware, software, services, manufacturing, and SaaS.

- IP & Competitive Moat – Across the portfolio, there are over 30 patents as well as extensive trade secrets and proprietary operating platforms.

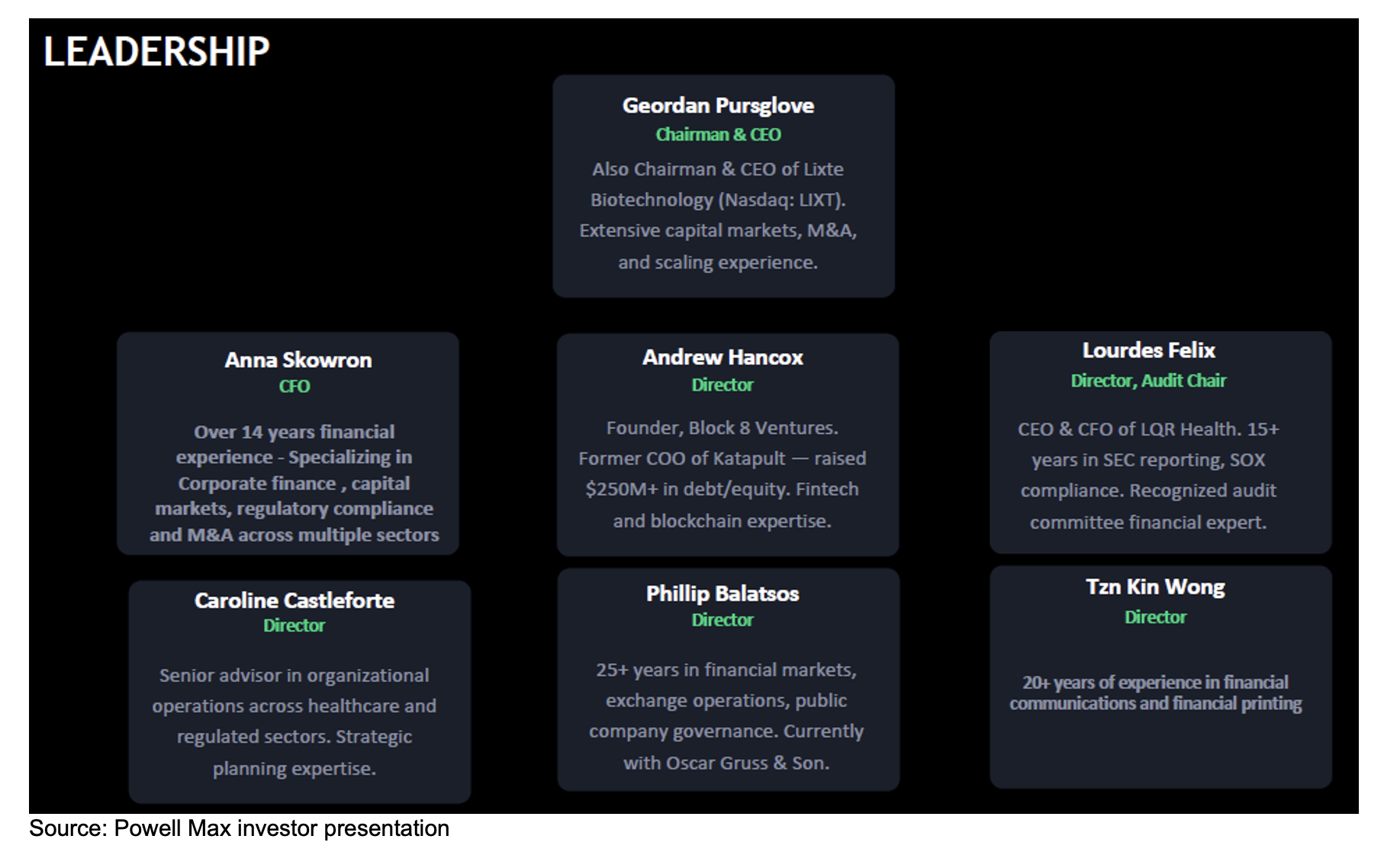

MANAGEMENT

The Powell Max leadership team has extensive experience across M&A, corporate finance, capital markets, regulatory compliance, and scaling businesses in multiple sectors.

SUMMARY

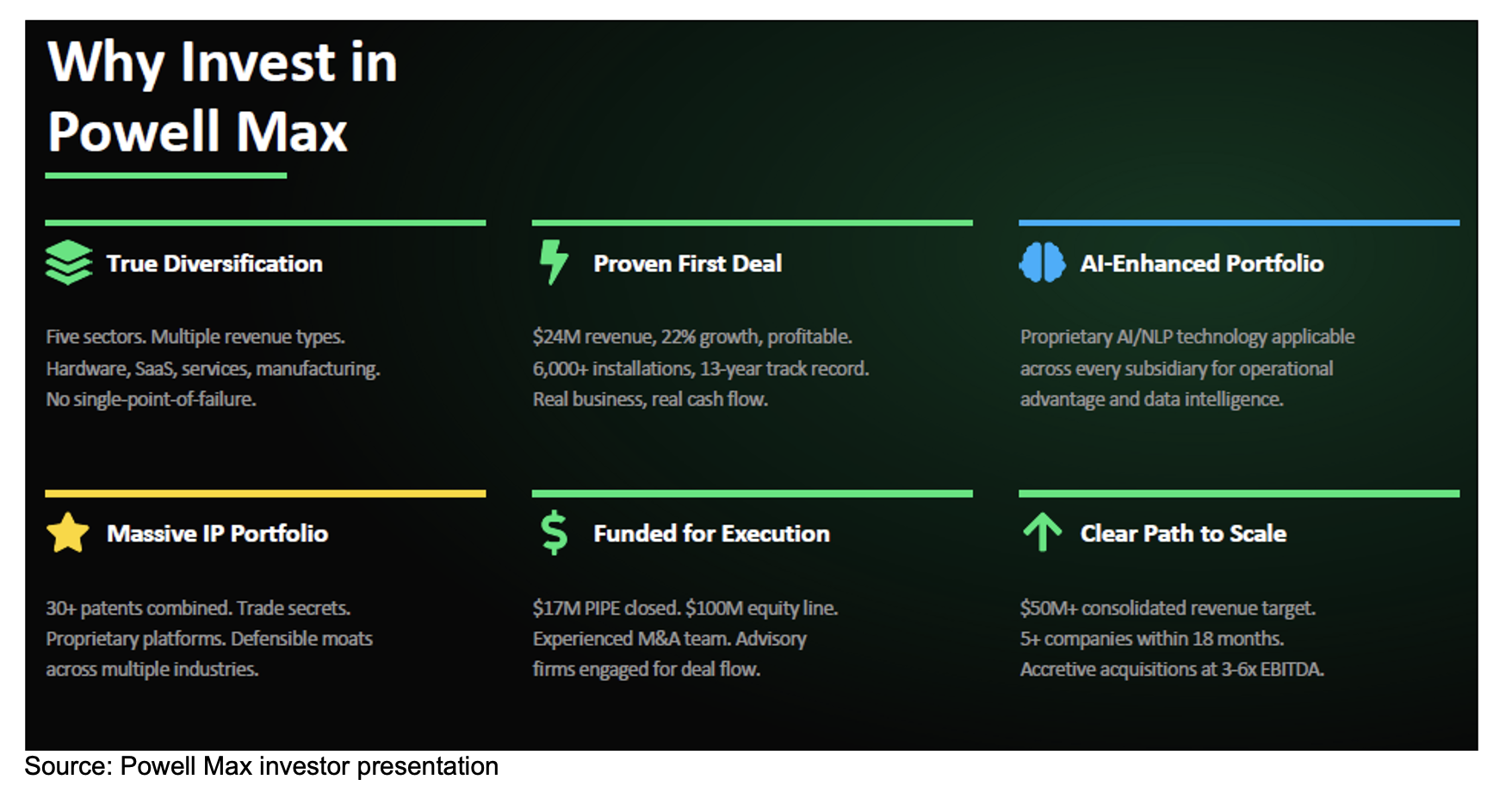

Powell Max is building a diversified portfolio of companies across five sectors with exposure to multiple revenue streams, including hardware, SaaS, services, and manufacturing. This will reduce concentration risk and limit single-point-of-failure exposure.

The company has already announced a proven first transaction featuring a profitable business with approximately $24 million in revenue, 22% revenue growth, more than 6,000 installations, and a 13-year operating track record. This provides an established cash-flowing foundation for the broader platform. Management’s strategy centers on assembling an AI-enhanced portfolio of operating businesses, leveraging proprietary AI and NLP capabilities across subsidiaries to drive operational efficiencies, improve decision-making, and unlock portfolio-wide data intelligence.

The investment case is further supported by meaningful intellectual property and a defined capital-backed acquisition strategy. Across the proposed portfolio, Powell Max is targeting businesses with defensible competitive positions, including over 30 combined patents, trade secrets, and proprietary technology platforms that create durable moats across multiple industries.

With a $17 million PIPE completed and an experienced M&A team supported by external advisory firms, the company appears well positioned to execute its roll-up strategy. Powell Max is targeting a clear path to scale through accretive acquisitions at 3x–6x EBITDA, with a stated objective of exceeding $50 million in consolidated revenue and building a portfolio of more than five companies within 18 months.

Investors may have the rare opportunity to get in on the ground floor of an emerging conglomerate that will continue to compound investor returns over the long term.

SUBSCRIBE TO ZACKS SMALL CAP RESEARCH to receive our articles and reports emailed directly to you each morning. Please visit our website for additional information on Zacks SCR.

DISCLOSURE: Zacks SCR has received compensation from the issuer directly, from an investment manager, or from an investor relations consulting firm, engaged by the issuer, for providing research coverage for a period of no less than one year. Research articles, as seen here, are part of the service Zacks SCR provides and Zacks SCR receives payments totaling a maximum fee of up to $50,000 annually for these services provided to or regarding the issuer. Full Disclaimer HERE.