By Brian Lantier, CFA

NASDAQ:RENX

READ THE FULL RENX RESEARCH REPORT

- RenX Enterprises Corp. (Formerly Safe and Green Development Corporation) (NASDAQ:RENX) has shifted its focus significantly in the past year, and, following the acquisition of Resource Group in June 2025, the company is now focused squarely on producing engineered soils, organic waste processing (composting), and offering logistics services for recyclables, organic, and municipal solid waste.

- In 2025, RenX began transitioning away from the real estate development business it previously operated and focused on developing its business lines within Resource Group. While the company still retains ownership interests in several real estate development projects and any sales of these interests could improve the company’s financial condition, investors should expect the management to focus on the organic recycling and logistics business going forward.

- The company indicated that Resource Group had revenues of approximately $18.15 million in 2024. While there is a fair amount of seasonality in the business and variability tied to weather-related cleanups, long-term municipal contracts should provide some stability to the company’s revenue stream.

- The lack of severe weather events in the Tampa, Florida, area has likely impacted 2025 results, as 2024 saw several severe weather outbreaks in the area. Additionally, US immigration policy changes and rulings on driver qualifications likely impacted the company’s driver pool for both the municipal solid waste and organic material businesses. We believe that the company’s core operations – Resource Group and its affiliated logistics business Zimmer Equipment - have a recurring business model that should generate $13 - $15 million in revenue per year. When weather events lead to greater cleanup activity in the Tampa area (as occurred in 2024), revenues will likely exceed these core levels. Finally, if the new Microtec grinder successfully produces a high-value peat alternative and the company increases its sales of bagged products, we believe that revenues could grow meaningfully in the coming years, and margins should materially improve.

- RenX has a history of reported net losses and is unlikely to be cash flow positive in the next two years, so the risk of further dilution to existing investors is high, and execution risk remains substantial given the material shift in the company’s focus.

COMPANY OVERVIEW

As a result of the 2025 acquisition of Resource Group US, RenX's primary operations include engineered soil production, organics processing, and logistics infrastructure for organic material collection, municipal solid waste, and recyclables. RenX's management is investing in additional technologies to produce organic material, which could eventually improve margins and boost sales in 2026 when the equipment comes online. We will discuss these initiatives later in the report.

Resource Group US

This business represents one of the company's core operating assets and offers materials processing, mulch production, and engineered soils to customers. The company creates customized soil and compost products for agricultural production and commercial real estate customers.

The company operates a borrow pit (a large, excavated site where organic waste can be disposed of and allowed to break down over time) and a green waste recycling facility.

The company now operates several trucks, walking floors, grinders, and other heavy equipment to process up to 500,000 tons of material at its 81-acre facility.

RenX, through its Resource Group division, utilizes both static pile composting (where material is piled and broken down by bacteria) and windrow composting (where large rows of material are mechanically turned to increase decomposition).

During our site visit to the company's Myakka, Florida, facility (roughly 60 miles outside of Tampa), we noted the large quantities of material being held pending the installation of new equipment. The company anticipates processing woody debris with a new milling technology from Microtec (a related company to Resource Group) that will produce a nutrient-rich material that can be used as an alternative to peat. The company believes that the new growing media will have desirable water retention and aeration characteristics demanded by its customers. Providing a locally sourced alternative to peat could be a strong point of differentiation for Resource Group in the market. However, the grinding equipment ordered from Microtec has not yet been installed. Once installed in 2026, the company's output will still be relatively new and will require longer-term testing before buyers are likely to commit to greater outputs. The company's ability to offer high margin bagged soil blends, compost, and growing media is a key component of our growth expectations.

For the three months ended 9/30, RenX reported that the Resource Group division recorded roughly $760,000 in revenue, or just over 20% of the company's total revenue. However, due to the substantial value-add of the company's finished products, the gross margins in this business are extremely high (60%). Thus, this business accounted for roughly half of the total gross profit despite its much smaller share of total revenue, and it is possible that these margins could expand further once the new Microtec grinder is installed in 2026. We anticipate that over time, the Myakka facility will account for the majority of the company’s gross profit.

Zimmer Equipment Inc. (ZEI)

RenX, through its Resource Group Products & Logistics division, operates a fleet of more than 50 tractor-trailer units capable of collecting and hauling municipal solid waste, green yard waste (primarily grass clippings), limbs/trees, and other organic material from municipal, corporate, and landscaping clients. The company also operates several transfer stations where it collects green waste before transporting it to the company's processing facility. Zimmer Equipment works closely with Waste Connections (NYSE: WCD), the $40 billion waste company, to transport municipal solid waste and recyclable material to other sites for processing.

The company also uses its fleet of vehicles to make outbound deliveries of finished products, such as compost, mulch, or potting mixes, to customers. Zimmer Equipment has long-term contracts in place with municipalities like the City of St. Petersburg and Hillsborough County, Florida, which is home to 1.6 million residents.

Zimmer Equipment recorded revenues of $2.76 million in the three months ended 9/30/25, representing nearly 80% of the company's total revenue in the quarter. The competitive nature of the transportation market means the company realizes smaller margins (just 16.6% gross margins in the latest quarter), so while this division accounts for the bulk of the company's revenues, it produced just about half of the gross profit in the third quarter.

Legacy Property Development Business

From the company's founding in 2021 through 2023, its primary focus was on acquiring land for residential development (single-family and multifamily projects). This legacy business ultimately acquired properties based in Texas, Georgia, and Oklahoma.

The company has undergone a significant shift in priorities following the acquisition of the Resource Group. While management has stated that it will continue to "identify land and development opportunities that support long-term economic value," we do not expect this to be a meaningful contributor to the company's future operating revenues.

The company engaged CBRE, a real estate valuation firm, in June 2025 to evaluate two properties:

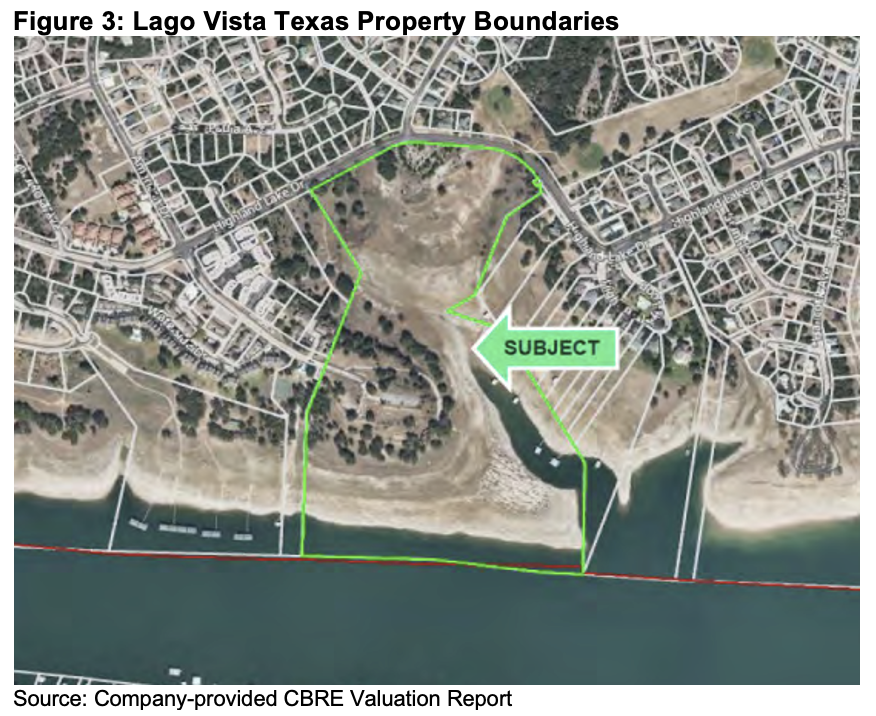

▪ Lago Vista, Texas: Roughly a 59-acre site on Lake Travis outside of Austin, Texas.

In Figure 3, we can see that this undeveloped property has roughly 700 feet of waterfront on Lake Travis. While approximately 70% of the land is designated as Flood Zone AE (1% annual risk of flooding), many adjacent properties have been developed by building closer to the road, leaving the land along the waterfront for dockage.

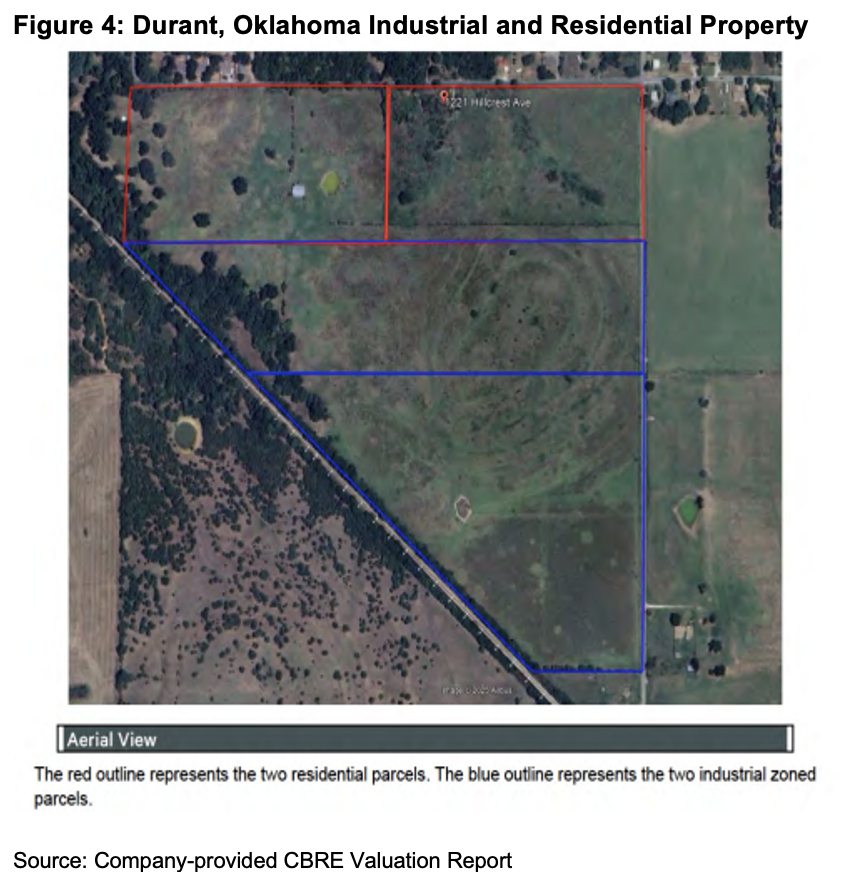

▪ Durant, Oklahoma: Roughly 113-acre site in Bryan County, Oklahoma, about 80 miles north of Plano, Texas, a mid-sized suburb of the Dallas/Fort Worth metropolitan area. This property has roughly 46 acres zoned residential and approximately 68 acres zoned industrial.

CBRE appraised the Lago Vista, Texas, property at $6.4 million ($108k per acre) and the Durant, Oklahoma, property was valued at $3.5 million (approximately $31k per acre) in June 2025 for a combined value of $9.9 million of real estate assets.

The company also owns a 7 acre property roughly 5 miles outside of Atlanta in East Point, Georgia that is currently an undeveloped property. The company had an independent valuation of the property conducted in 2024 and the property was valued at $1.7 million. Land prices have softened a bit in this region but given the proximity of the property to regional transportation centers and downtown Atlanta we believe it will still be attractive to developers.

In early January 2026, the company announced that it had restructured a $7 million secured note on the Lago Vista property by transferring title to the lender in exchange for the conditional extinguishment of $5 million of the secured note. The company also noted that $2 million of the remaining balance has been secured against the Durant, Oklahoma, property, which the company intends to market for sale in 2026.

In 2023, Resource Group had an independent appraisal conducted of the Myakka facility, which included a valuation of the potential sand reserves on the property. At the time, it was estimated that the property had roughly 9 million tons of sand reserves. The appraisal firm estimated that, based on its analysis, the ground reserves could be valued at roughly $1.10 per ton, which would give the total reserves a value of almost $10 million. Since the time of this appraisal, sand prices have generally increased in the Florida market, so it is likely that the total value of these reserves has also increased.

We think it would be prudent for investors to consider that these real estate assets may eventually be sold at a price potentially lower than the CBRE estimate. However, even at a 10-20% discount to the CBRE estimate, the sale of these properties should still eliminate the associated debt, and the value of the sand resources at the Myakka facility offers potential upside if the company elects to tap into this asset.

MANAGEMENT

David Villarreal, President/CEO

Mr. Villarreal has been the President and CEO of RenX since early 2023, and he has been a director of the company since 2021. Mr. Villarreal previously served as the Chief Administrative Officer of Affinity Partnerships, the referral program operated by Costco that provided Costco members with access to a network of 10 national mortgage lenders. The lenders offered capped fees and lower origination costs on various home loans to Costco members. The program supported annual closed loan production of more than $8 billion. Before this role, Mr. Villarreal was the President of Corporate Business Development at Prime Source Mortgage, Inc.

Nicolai Brune, CFO

Mr. Brune has served as RenX's CFO since early 2023. Prior to assuming this role, Mr. Brune was the Director of Acquisition for RenX (then known as Safe & Green Holdings Corp), where he was responsible for financial evaluation and modeling of potential acquisitions, investments, and divestitures.

Before joining RenX, Mr. Brune served as a treasury analyst at GL Homes, a private real estate developer in Florida, from June 2020 to March 2022.

Given the significant shift in RenX's operational focus from real estate development to the production of engineered soils, mulch, and transportation services, it is important to note that management at Resource Group has continued to manage operations subsequent to RenX's acquisition of Resource Group.

Anthony Cialone, CEO, Resource Group

Mr. Cialone has served as the President and Chief Operating Officer of Resource Group since 2019, during which he has led the company to become a regional leader in converting yard waste into compost and to establish a transportation infrastructure to create a closed-loop system. Mr. Cialone also serves as the President of Microtec (the company that has sold a RenX, a significant new milling technology) and the CEO of AggrePlex, which produces ground glass pozzolan, a finely ground, recycled waste glass that is used as a sustainable supplement in concrete.

Importantly, both Resource Group and Zimmer Equipment have experienced operational managers who run day-to-day operations, and we believe these individuals will be key to RenX's success in this pivot.

INDUSTRY OUTLOOK

Given the shift in RenX's focus to engineered soils, mulch, and material transportation, it's relevant to review these markets. Trends in engineered soils have been toward greater precision in soil composition and increased customization of the soil's physical and chemical properties for the intended end use. The primary uses of engineered soils are to improve yields, conserve resources such as water, and reduce erosion or topsoil loss. The market for mulches has remained little changed in recent years, but there has been increased emphasis on the sustainability of materials, and color additives for mulch have become a popular trend in residential use.

While it is difficult to forecast demand growth rates for RenX's principal products and logistics services because of the fragmented nature of this market, we anticipate that the manufactured soil and mulch markets will continue to demonstrate strong demand in the foreseeable future, assuming the US economy continues to expand. The company's logistics business has a baseline of business from customers with long-term contracts, but historically, it has experienced strong outperformance during periods of inclement weather that require additional cleanup vehicles. While it's impossible to forecast demand associated with post-storm cleanups, we do think that it is more likely than not that the company's core markets will experience significant weather events in the coming years that could drive additional one-time demand.

The market for composting and organic recycling is primarily controlled by national waste management companies like Waste Management and Republic Services, with almost all markets having a variety of municipal and private composting providers that collect organic materials. The drive to reduce waste that could be composted and increase the sustainability of our waste systems has led many municipalities, including large cities like New York, to enforce composting rules for the first time in 2025. It is unclear whether these trends will remain a priority for municipalities in the current political climate, but we believe many municipalities will continue to roll out composting initiatives because they are popular with citizens and can clearly reduce total waste volumes.

Specifically in the markets where RenX operates (the Gulf Coast of Florida), the demand for engineered soils and mulch is mainly driven by the agricultural markets that include nurseries, strawberry production (the region accounts for almost 15% of the nation's strawberry output and nearly 100% of the winter output), and other vegetables like tomatoes, watermelon, and zucchini. The soil in this region tends to be sandy and low in organic matter, so engineered soils are critical to enhancing the production of fruits and vegetables.

There are several companies (all privately owned) that operate in this market and have long-standing relationships with the region's growers, including:

- The Mulch and Soil Company - operating four facilities across the state.

- Amerigrow – part of the McGill Compost group, which operates seven facilities in 6 different states.

- Southeast Soils – operates a single 20-acre facility in Florida

- Veransa Group – operates several facilities in Florida that provide compost, mulch, and soil blends.

Much of the company’s mulch is sold directly to wholesalers or landscapers, while some is sold to large mulch manufacturers who then dye the product and bag it for retail sale. Trends in the industry continue to move toward closed-loop recycling systems that enable the production of soil and mulch locally, thereby limiting the carbon footprint of their production.

Broadly, demand for engineered soils, compost, and mulch in the Florida area will be driven by increased use of sustainable agricultural practices, greater awareness of soil health, and local initiatives to encourage water conservation. Increased urban development in the region (we saw many new housing developments under construction within 20 miles of the Myakka facility) and greater organic waste recycling efforts should also drive demand for established companies operating in this industry in Florida.

BUSINESS MODEL

RenX Enterprises' business model is now focused on the organic recycling, composting, engineered soil, and mulch products produced by its Resource Group acquisition, as well as the trucking/logistics operations of Zimmer Equipment.

The core of the RenX business model lies in converting organic waste (grass clippings, wood debris) into high-value products, such as engineered soils and mulch, for agricultural and landscaping customers. The company's business is similar to many "waste-to-value" recycling companies that seek to increase the value of the waste products rather than just collecting disposal fees. By integrating waste collection and transportation with waste processing, RenX is able to secure consistent access to feedstock materials, and the fleet of trucks operated by Zimmer Equipment ensures regular pickup and delivery.

The company's finished products are sold principally to agricultural customers and landscapers/golf courses, and its organic waste collection services are used primarily by municipalities. Compost is also sold to nurseries, vegetable growers, open-field producers (beans, corn, sugarcane), citrus growers, and bagged for retail customers and garden centers.

Growth Opportunity

The addition of a new grinder from Microtec could enable the company to create a high-value peat alternative. The success of this new product in the market will likely be a key growth driver for RenX. As part of this initiative, the company has also invested in a new bagging and blending system at the Myakka facility, enabling it to sell retail-ready products.

Additionally, the company has invested in new processing machinery that should significantly increase the facility's throughput and the quality of the final product. We predict that the majority of the gross volume of products shipped from Myakka will still be mulch and compost which have fairly low price points around $30-40/ton, but the new blending lines, Microtec grinder and onsite bagging will enable the company to sell premium blended soils and substrates that can command prices of up to or beyond $150/ton (4-5 times the standard mulch/compost price). The potential to generate up to 5 times the revenue from the same source material has significant implications for topline growth and profitability.

RECENT NEWS

- In June 2025, RenX (then known as Safe and Green Development) announced that through its Resource Group subsidiary, it had secured an exclusive license to deploy a milling technology from Microtec Development Holdings. To date, Microtec has focused principally on "waste-to-value" applications in the glass and concrete markets with more than 250 mills installed. The company believes that products produced by this mill could provide a domestic alternative to Canadian and Florida peat and coconut husks. At the time of the initial press release on this mill, the company indicated that, due to the composition of this product, it could realize pricing of up to $150/ton, which would be up to 5 times current market compost prices. In June 2025, this mill was projected to be delivered and installed in the third quarter of 2025; however, in December 2025, the company updated the timeline and now expects commercial deployments in 2026, with the first delivery of the Microtec mill in March 2026.

- In December 2025, RenX announced that a new customer issued multiple purchase orders for wood fines (small wood by-products like sawdust, barkdust, or splinters that are generally smaller than ¼"), which would equate to roughly $9,000 per week from this customer, and the company expects orders to continue at this rate. Given that we estimate total revenue from the Resource Group's soil/compost division was only $58k per week in the most recent quarter, this new customer represents a significant uptick in revenue, potentially accounting for up to 15% of soil/compost revenues in 2026.

- In October, the company completed a private placement that raised $8.15 million of net proceeds. The offering consisted of roughly 6.6 million shares of common stock at $1.36 and another 6.6 million warrants exercisable at $1.36. Prior to this financing, the company reported 8.8 million shares outstanding; however, several adjustment provisions in the private placement could materially impact the total share count if certain events occur. If all the anti-dilution and adjustment shares and warrants were issued, the company's total share count could increase from 8.8 million to roughly 100 million. At this time, the company has not updated the total outstanding share count, but the stock is currently trading below the floor price that would trigger additional share issuance if the company were to complete additional financings. We think the total number of shares issued could ultimately be lower than 91.9 million, but the possibility of such extreme dilution is creating significant uncertainty around the shares. We believe the company's current share count is around 36 million, based on our calculations using publicly disclosed information.

Given the company's history of losses and limited financial flexibility, investors should take the risk of future dilutive financings seriously.

- In June 2025, RenX completed the acquisition of Resource Group in exchange for $480,000 (in the form of a promissory note), restricted common stock equal to 19.99% of the company's common stock as of the closing (we estimate this to have been roughly another 400,000 shares), and 1.5 million series A convertible preferred shares that is convertible into 9,000,000 restricted shares of the company's common stock.

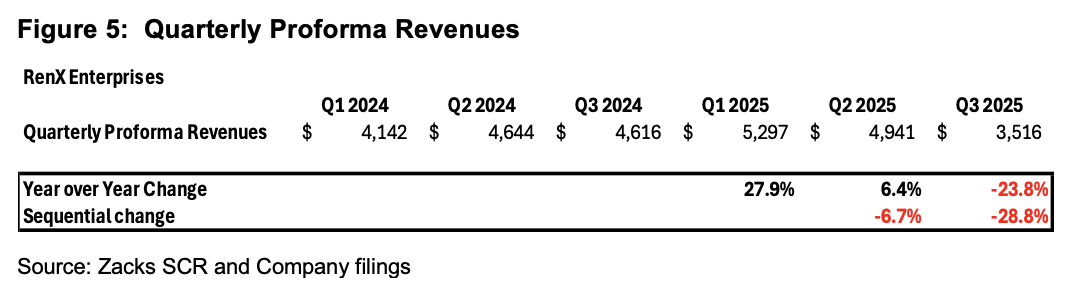

- In November, the company reported its first full quarter of operations after the acquisition of the Resource Group. While the headline revenue number was impressive at $3.5 million (up more than 4,000% from actual results in the same quarter of 2024), it is important to note that this is not an apples-to-apples comparison, as the acquisition of Resource Group in the second quarter meant that the results for the quarter included Resource Group for the first time. By reviewing the quarterly pro forma results disclosed in RenX's (then Safe and Green Development) 10-Qs, we can get a clearer picture of the company's revenue patterns.

It is worth noting that despite the fairly consistent performance in 2024, revenues in 2025 have significantly underperformed the company's initial forecasts. When the transaction was announced, RenX indicated it anticipated 2025 pro forma revenues of $25 million, yet after nine months, pro forma revenues are just $13.7 million and actually fell year over year and sequentially by more than 20% in the third quarter. The lack of any significant weather events in the Tampa area in 2025 (and the related weather cleanups that would have accompanied them), machinery upgrades at Myakka, and driver availability issues likely impacted 2025 results and led to the revenue decline in the third quarter. We also believe that the company anticipated operating the Microtec milling operation in 2025, which could explain a meaningful portion of the disparity between the initial pro forma expectations and actual results.

In early January 2026, RenX reported that 2025 revenues for the combined company are expected to be approximately $7 million. While this is a marked improvement over the reported revenue of less than $500k in 2024, it is important to note that RenX previously stated that the Resource Group's revenue was roughly $18.15 million in 2024. With revenues averaging about $1 million per month in 2025, compared to roughly $1.3 million and $1.5 million in 2023 and 2024, it appears the lack of major weather events in 2025, equipment upgrades at the Myakka facility, and challenges associated with driver availability impacted 2025 results. We believe the company's base-case revenue run rate is about $15 million, and upside to this base level will be driven by the sale of new products produced at the Myakka facility.

Also, in January 2026, as noted above, the company agreed with its lender to assume title to its largest real estate asset in Texas in exchange for the conditional elimination of $5 million of debt.

In January 2026, RenX engaged Mr. Bob Jacobson as a Strategic Business Development Advisor to its renewable materials and engineered soils product lines. Mr. Jacobson's expertise will be leveraged to establish and deepen relationships with nationally recognized growers and bagged-goods partners. Mr. Jacobson has had an extensive career in large-scale retail garden operations and spent more than twenty years at The Home Depot.

Finally, in February 2026 the company announced that it had restructured its investment in the Norman Berry property in East Point, Georgia converting its initial equity investment of $600k into a secured note while retaining an ownership interest. This new structure prioritizes the return of capital to RenX while retaining exposure to any upside in the property’s sale. In late 2025, RenX secured additional zoning entitlements for the property which broadens the potential uses for the property and this should increase the pool of possible buyers.

EARNINGS OUTLOOK

In previous releases, management at RenX reported pro forma revenues for RenX's operating entities (Resource Group and Zimmer Equipment) through the first nine months of 2025 were $13.8 million. Given the preannounced full-year revenue of "more than $7 million," we are projecting a sequential decline in fourth-quarter revenue to roughly $2.5 million. We anticipate full-year pro forma revenue of just over $16.2 million, representing a year-over-year decline of more than 10%. However, we recognize that this preannouncement may have simply involved the company issuing conservative guidance.

We anticipate that gross margins for the Resource Group business will remain above 60%, but those for the Zimmer Equipment transportation business will stay below 20% due to the commodity nature of short-haul trucking. While we forecast the company will work to control operating costs, we still expect 2026 and 2027 operating expenses to exceed $13 million each year.

We forecast that the company will continue to incur significant interest expense of at least $4.7 million in both 2026 and 2027 despite the reduction of debt associated with the Lago Vista transaction. If the company can sell its existing real estate holdings, it could significantly improve its financial condition. At this point, our estimate for fully diluted shares outstanding is highly uncertain, and we believe we will have a better understanding of the total share count when the company's 10-K is filed in March. We are estimating a fully diluted share count of 36 million today.

We forecast that revenues will stabilize in 2026 as new equipment is added at the Myakka facility and driver availability improves. Our revenue forecast for 2026 is $17.2 million, but we recognize it could be conservative if the company can sell a higher percentage of engineered soil products and substrates. We assume greater customer penetration for new products in 2027, and our revenue forecast jumps 54% to $26.4 million. We are also projecting a meaningful increase in gross profit, driven by higher sales of higher-margin soil products, with gross margins exceeding 40% in 2027. There is significant uncertainty regarding pricing and customer adoption of the company's new products, and any model will need to be adjusted as they enter the market.

While the company does approach operating breakeven in 2027 in our current model (posting an operating loss of $2.6 million), it will still have significant interest expense unless debt is extinguished through asset sales.

There are several unknowns in our model, including total share count, and investors should be prepared for the potential for future dilution if the company utilizes equity markets to fund operations, and anti-dilution provisions in prior financings kick in.

RISKS

Potential failure to satisfy NASDAQ listing requirements – Shares of RenX have traded sharply below the NASDAQ minimum closing bid price of $1.00 per share since early December. If the company’s shares continue to trade below $1.00, it could risk delisting or consider options such as a reverse split to maintain its listing.

Dilution Risk – As of October 29, 2025, the company had 8.8 million shares outstanding, but we believe the total share count could grow to nearly 100 million if all warrants were exercised and anti-dilution provisions were triggered. Additionally, the company has significant near-term debt and negative operating cash flow, which will likely require equity issuance to sustain operations. The risk of future dilution for existing shareholders is very high.

Going concern risk – The company’s auditors have expressed substantial doubt about our ability to continue as a going concern.

Multiple business pivots – The company was founded in 2021 and has shifted from land development and modular property construction to real estate-related AI technology, then to composting, engineered soils, and logistics in 2025. The number of significant shifts in the business creates a risk that the management team may not be able to properly execute the business model.

Competitive risk – The company’s primary markets, composting, engineered soils, and logistics, are highly competitive industries, and the commoditized nature of many of the company’s products could limit its pricing power in the market.

SUBSCRIBE TO ZACKS SMALL CAP RESEARCH to receive our articles and reports emailed directly to you each morning. Please visit our website for additional information on Zacks SCR.

DISCLOSURE: Zacks SCR has received compensation from the issuer directly, from an investment manager, or from an investor relations consulting firm, engaged by the issuer, for providing research coverage for a period of no less than one year. Research articles, as seen here, are part of the service Zacks SCR provides and Zacks SCR receives payments totaling a maximum fee of up to $50,000 annually for these services provided to or regarding the issuer. Full Disclaimer HERE.