By John Vandermosten, CFA

NASDAQ: RVPH

READ THE FULL RVPH RESEARCH REPORT

Crosswinds have been gusting across Reviva Pharmaceutical Holdings, Inc.’s (NASDAQ: RVPH) runway over the last year but have dissipated recently, allowing for another transit down the taxiway. In December, the FDA recommended that brilaroxazine undergo a second Phase III study in schizophrenia, dashing hopes that existing data would be sufficient to support a new drug application (NDA). Since then, Reviva has resumed plans to conduct its RECOVER 2 Phase III trial. To support the effort, the company has raised an additional $10 million gross in a public offering, plus an additional amount through the use of its at-the-market (ATM) facility and from the exercise of warrants. In its 2025 earnings update, Reviva highlighted its March cash balance of $23 million and outlined the timeline for RECOVER 2. The company expects trial initiation in mid-2026, patient enrollment in 3Q:26, and trial completion approximately one year after enrollment begins. A readout is anticipated a few months after the last patient, last visit, setting Reviva up for a 2028 NDA. Reviva’s flying machine is moving down the taxiway, preparing for a 2Q:26 takeoff.

Operational and Financial Results

On March 30th, 2026, Reviva reported 2025 financial and operational results and filed its Form 10-K with the SEC. Reviva generated no revenues in 2025 and posted an operational loss of $19.9 million with expenses primarily related to RECOVER’s OLE. For the year ending December 31st, 2025, and versus the same, prior year period:

- Research & development expense totaled $11.7 million, down 49% from $22.9 million, with the change attributable to lower external research and development costs and a shift towards lower-cost post-data readout activities and trial wind-down efforts;

- General & administrative expenses totaled $8.5 million, rising 8% from $7.9 million on account of higher stock-based compensation and legal expenses, partially offset by lower consultant and professional expenses, with other expense categories remaining relatively flat;

- Other income of $354,000 compared to $900,000, with the difference almost entirely attributable to a lesser magnitude gain on remeasurement of warrant liabilities. Net interest income is $298,000 vs. $343,000;

- Provision for taxes was $19,000 compared to $20,000 related to payment of state and foreign taxes;

- Net loss was $19.9 million vs $29.9 million, or $5.48 and $18 per share, respectively.

As of December 31st, 2025, Reviva held $14.4 million in cash on its balance sheet. 2025 cash burn was $24.6 million, while cash flows from financing were $25.6 million. Financing transactions from a public offering, an ATM facility, and warrant exercise contributed to the total. Following the end of the year, additional funds were raised with ATM, warrant exercise, and public offering proceeds. Reviva estimates that cash on the balance sheet was $23 million following the March 20th, 2026, public offering close. The company estimates that the balance is sufficient to start the RECOVER 2 trial and to support operations into 1Q:27.

Clinical Vocal Biomarker Publication

In January, Reviva announced the publication of vocal biomarker data in Biological Psychiatry. The article, entitled A Single, Interpretable Vocal Biomarker for Enriching Antipsychotic Clinical Trials, discusses how using a vocal biomarker can help enroll patients more likely to benefit from therapy.

Investigators used audio recording to evaluate speech latency in schizophrenia patients as part of Reviva’s Phase III RECOVER trial evaluating brilaroxazine. The approach evaluated 2,320 recordings from 406 participants with acute psychosis from three countries speaking eight languages. Patients who expressed moderate to severe negative symptoms, as measured by the PANSS, showed longer speech latencies, with large effect sizes across country and language subgroups. 180 patients were identified as vocal biomarker (VBM) negative, and 228 were identified as VBM positive. Patients administered Brilaroxazine showed statistically significant outcomes versus placebo from baseline to end of treatment in the VBM-positive group for nearly every outcome measure, despite having fewer participants. Treatment effects for VBM-positive patients were large for nearly every outcome measure.

Investigators observed that the speech latency-VBM is an objective biomarker derived from standard clinical assessments. The article concluded that using speech latency for enrichment could have reduced the required sample size by half while nearly doubling the observed treatment effect. The VBM offers a meaningful opportunity for reducing clinical trial costs and burden.

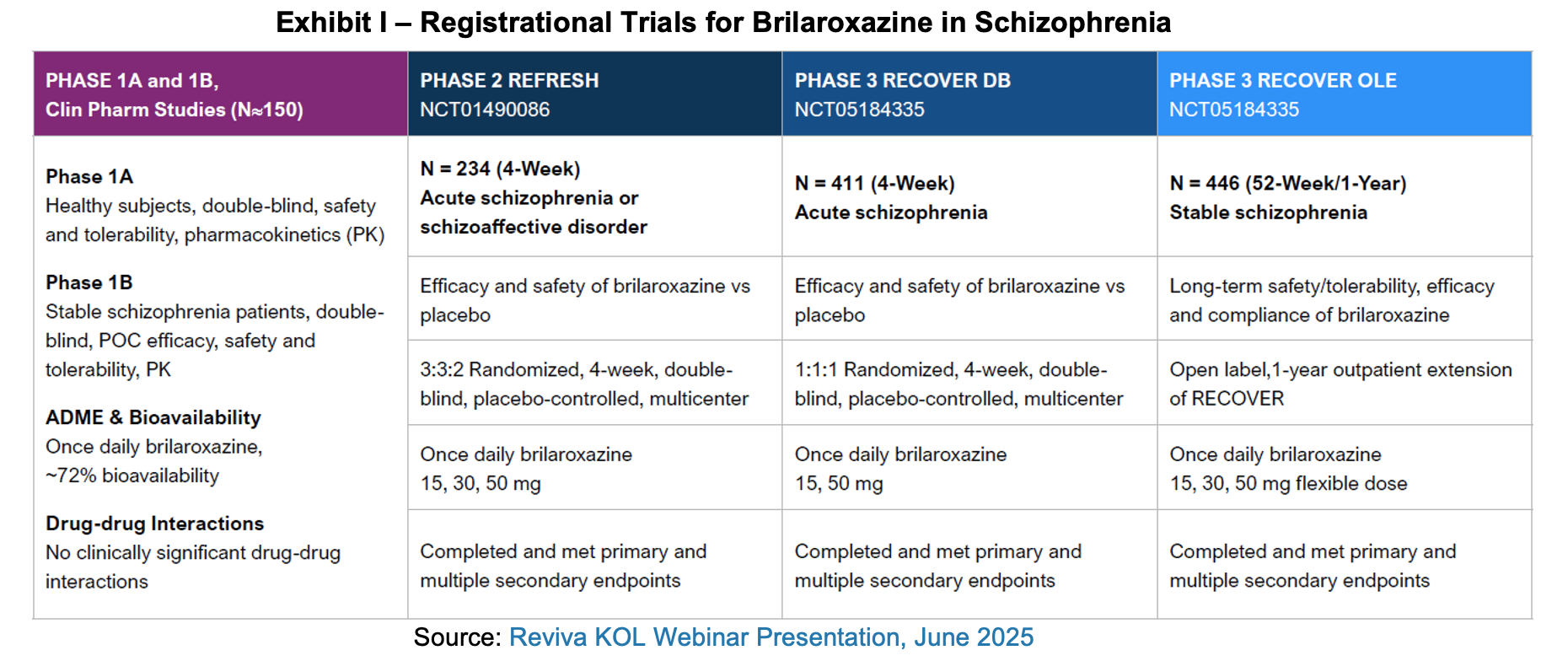

Regulatory Path

Reviva had explored the possibility of submitting an NDA supported with data from its Phase II and first Phase III study. However, in a written response provided to Reviva in December, the FDA recommended that a second Phase III study be conducted for brilaroxazine in patients with schizophrenia to generate additional efficacy data and expand the safety dataset. This response eliminated the possibility that the NDA could be filed with existing data. The FDA further provided Reviva with guidance for methods of data analysis, methods of data presentation, and data requirements for studies of animal pharmacokinetics, human abuse potential, and renal and hepatic impairment.

Reviva is looking at other alternatives to extend brilaroxazine’s patent life, including finding a closely related indication, such as one centered on the negative symptoms of schizophrenia, using a new, potentially more concentrated, formulation. It is also planning another trial that will focus on negative symptoms, an area where brilaroxazine differentiates itself from its peers. If successful and approved, this could establish Reviva’s drug as the go-to product for treatment of negative symptoms.

$10 Million Public Offering

On March 18th, Reviva announced a public offering, which was priced the same day. The deal closed on March 20th, 2026. The company sold 6,666,667 shares of common stock at $1.50 per share with two warrants attached to each share. One of the warrants is classified at a Series G warrant, which has an exercise price of $1.50 per share, is exercisable immediately, and offers a five-year life. The other warrant also has an exercise price of $1.50 per share and is exercisable immediately; however, it carries a shorter 12-month duration. The sale raised $10 million in gross proceeds, which will be used to start the second Phase III trial for brilaroxazine. The proceeds from this transaction will be added to the approximate $15 million that is on the balance sheet, which was augmented with warrant exercises from previous rounds.

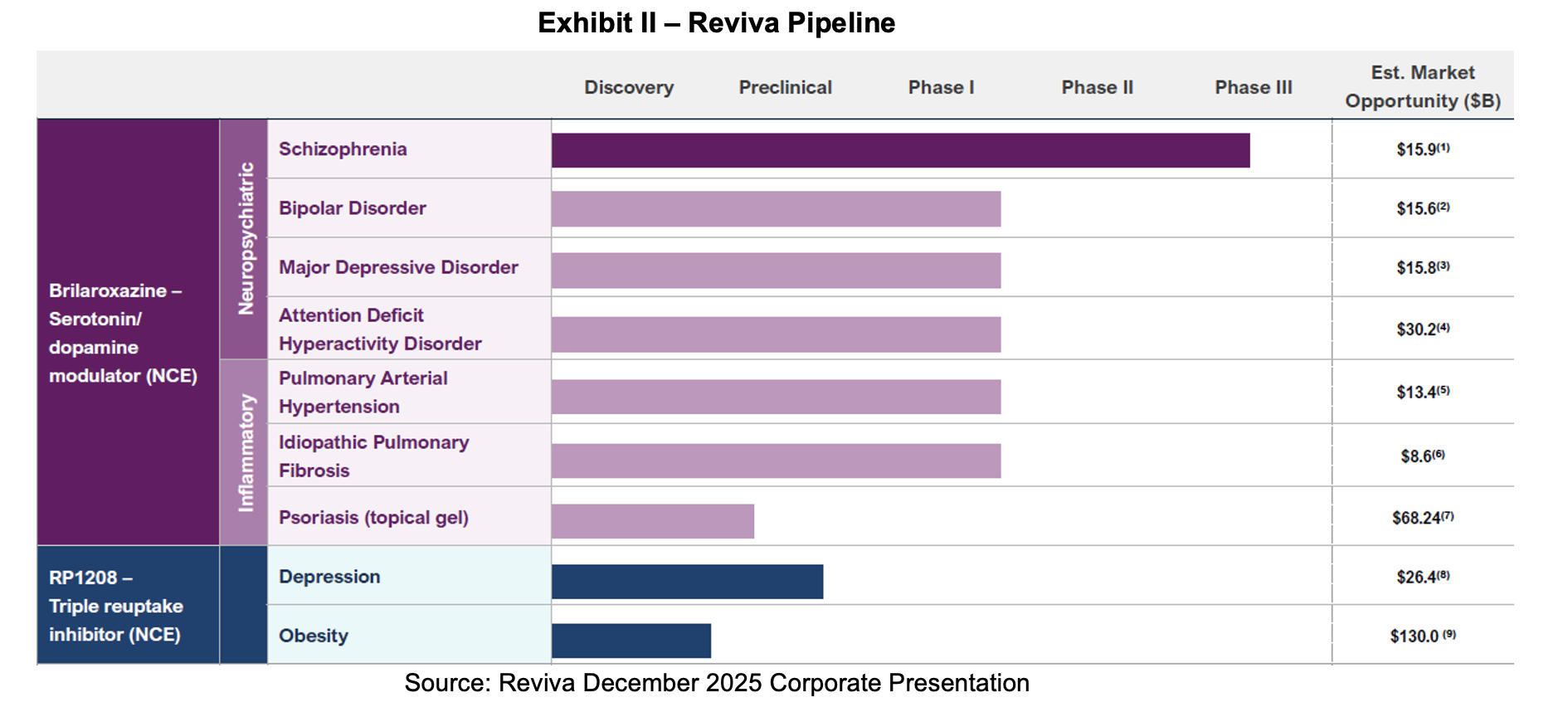

Company Pipeline

Milestones

- Full data released for OLE study – 2Q:25

- $9 million public offering executed – September 2025

- Lytham Partners Investor Conference participation – September 2025

- Roth Healthcare Opportunities Conference participation – October 2025

- Alliance Global Partners KOL Webinar – October 2025

- CNS Summit 2025 participation – November 2025

- Spartan Capital Securities Investor Conference participation – November 2025

- Brilaroxazine Pulmonary Fibrosis patent grant in Europe – November 2025

- Poster presentation at Neuroscience 2025 – November 2025

- Presentation at Sachs Neuroscience Innovation Forum – December 2025

- Publication of clinical vocal biomarker data in Biological Psychiatry – January 2026

- Launch RECOVER 2 Phase III trial – 2Q:26

- Enroll first patient in RECOVER 2 Phase III trial – 3Q:26

- Topline readout of RECOVER 2 Phase III trial – 2H:27

- Potential brilaroxazine NDA submission to FDA for schizophrenia – 2028

Summary

Reviva reported 2025 financial results, burning $24.6 million for the year as it wrapped up its OLE trial and prepared for the second Phase III RECOVER 2 trial. Now that the company has approximately $23 million in cash on its balance sheet following a capital raise, it will launch its trial in the next few months, and we expect the first patient to be enrolled by September of this year. Management anticipates that an additional $35 million will be required to fund its completion. We think the timeline as outlined by management is reasonable, with a 2Q:26 initiation of the trial, first enrollment in 3Q:26, and enrollment completion about one year later. Treatment lasts about a month, which suggests the trial could wrap up somewhere around the middle of 2H:27, followed by a readout around year end. This positions Reviva for an NDA submission in 2028. We update our model to reflect the revised timeline, claims on equity, and the future capital needs.

RECOVER 2 enrollment is expected to be relatively quick, given the experience that the team has with the trial design. In the meantime, we expect to see more journal and conference presentations extolling brilaroxazine’s features, which have shown improved performance and reduced side effects compared with other approved antipsychotics. While our confidence in brilaroxazine and its performance in treating schizophrenia has not wavered, Reviva has had a difficult time gathering sufficient funding to support the completion of required studies. With enough cash to get RECOVER 2 started, we are hopeful that the timeline will now stand firm and Reviva will catapult its Phase III to cruising speed.

SUBSCRIBE TO ZACKS SMALL CAP RESEARCH to receive our articles and reports emailed directly to you each morning. Please visit our website for additional information on Zacks SCR.

DISCLOSURE: Zacks SCR has received compensation from the issuer directly, from an investment manager, or from an investor relations consulting firm, engaged by the issuer, for providing research coverage for a period of no less than one year. Research articles, as seen here, are part of the service Zacks SCR provides and Zacks SCR receives payments totaling a maximum fee of up to $50,000 annually for these services provided to or regarding the issuer. Full Disclaimer HERE.