By M. Marin

NASDAQ:PYPD

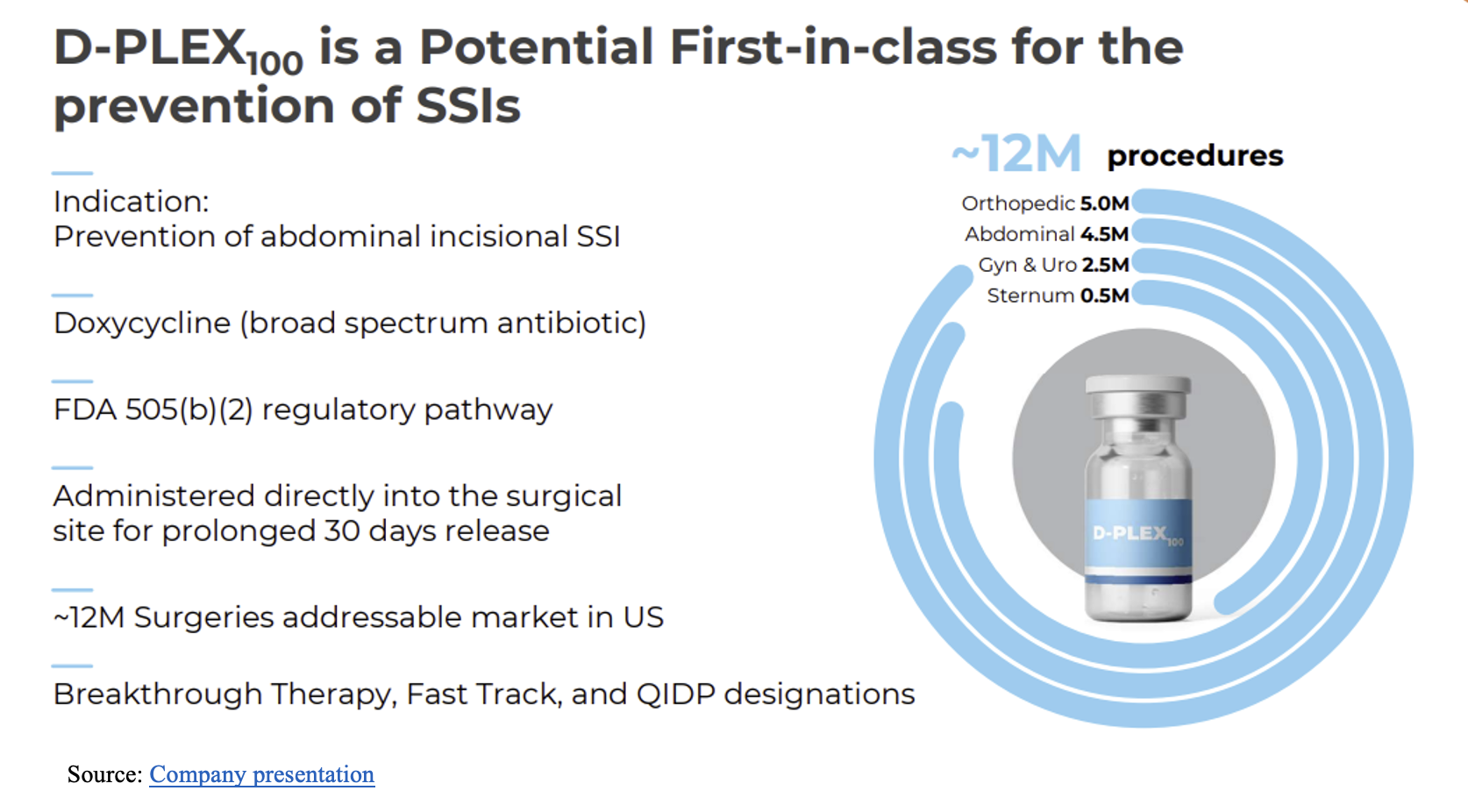

PolyPid Ltd. (NASDAQ:PYPD) is a late clinical stage biopharma company focused on developing locally administered, prolonged-release therapeutics using its proprietary Polymer-Lipid Encapsulation matriX (PLEX) technology. The PLEX delivery system is designed to improve surgical outcomes and enhance the efficacy of treatments while minimizing side effects, enabling the controlled delivery of medications directly at the surgical site over extended periods ranging from days to several months. PolyPid's lead asset is D-PLEX₁₀₀, a novel formulation intended to prevent surgical site infections (SSIs) in patients undergoing abdominal colorectal and potentially other surgery.

D-PLEX₁₀₀ Successfully Met SHIELD II Study Primary Efficacy & Key Secondary Endpoints

PolyPid conducted a pivotal Phase 3 clinical trial of D-PLEX₁₀₀, SHIELD (Surgical site Hospital acquired Infection prEvention with Local D-PLEX) II. SHIELD II is a randomized, double blind Phase 3 trial designed to assess the efficacy and safety of D-PLEX₁₀₀ alongside standard of care (SoC) therapies compared to SoC alone in preventing post abdominal-surgery incisional infection in patients with large incisions.

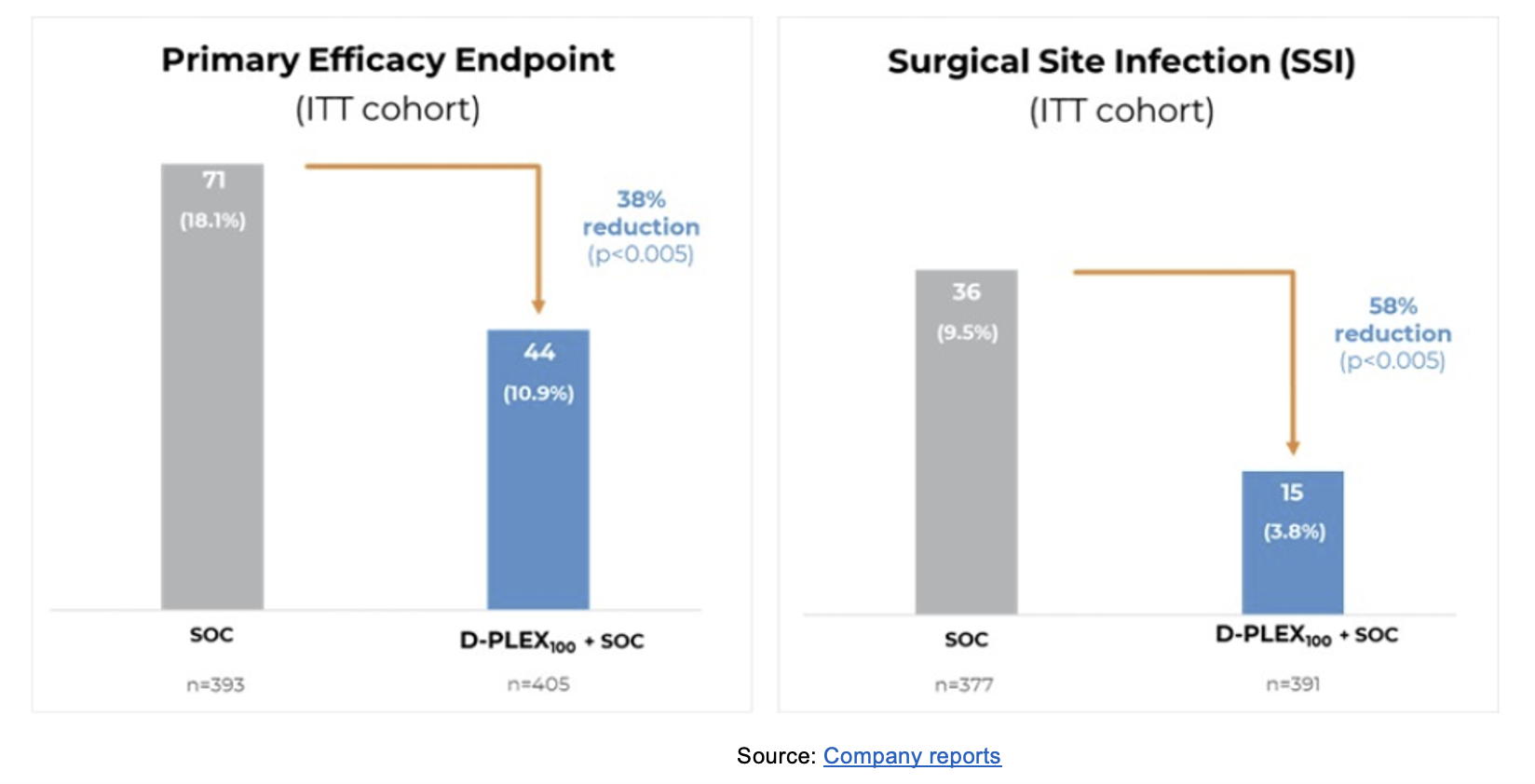

After completing enrollment of 800 patients in medical centers in the U.S., Europe, and Israel in the SHIELD II trial in March 2025, PolyPid reported top-line results last month. D-PLEX₁₀₀ successfully met the primary efficacy endpoint of the SHIELD II study, demonstrating statistically significant results (p<0.005) in 798 patients with large abdominal surgery incisions. Moreover, the SHIELD II trial included three key secondary endpoints and also demonstrated statistical significance in successfully meeting all critical secondary efficacy endpoints, including a 58% reduction in the rate of SSIs in patients treated with D-PLEX₁₀₀ compared to those treated with SoC (p<0.005).

The primary endpoint is the combination of deep and superficial SSIs, all-cause mortality, and surgical reinterventions at the same incision of the original index surgery. The second key secondary endpoint combined SSI, mortality, and reintervention as evaluated in the primary endpoint. This endpoint was assessed in the overall study population with an incision ≥7 cm, including laparoscopic surgery patients enrolled prior to a 2023 trial protocol change.

Key SHIELD II study findings - met primary and secondary key endpoints:

- Primary efficacy endpoint – significantly lower proportion of primary endpoint events among patients who received D-PLEX₁₀₀ plus SoC (n=405; 10.9%), compared to SoC alone (n=393; 18.1%), which represents a 38% reduction (p<0.005).

- First key secondary endpoint – 58% reduction in deep and superficial SSI rates among patients who received D-PLEX₁₀₀ plus SoC (3.8%) compared to participants who received SoC alone (9.5%) (p<0.005).

- Second key secondary endpoint – statistical significance in favor of D-PLEX₁₀₀ plus SoC over SoC alone (p<0.005).

- The third key secondary endpoint was met with a 62% reduction of patients with an ASEPSIS1 score >20 in D-PLEX₁₀₀ plus SoC arm compared to SoC alone arm (p<0.05).

SHIELD II Results on Primary Endpoint and First Key Secondary Endpoint

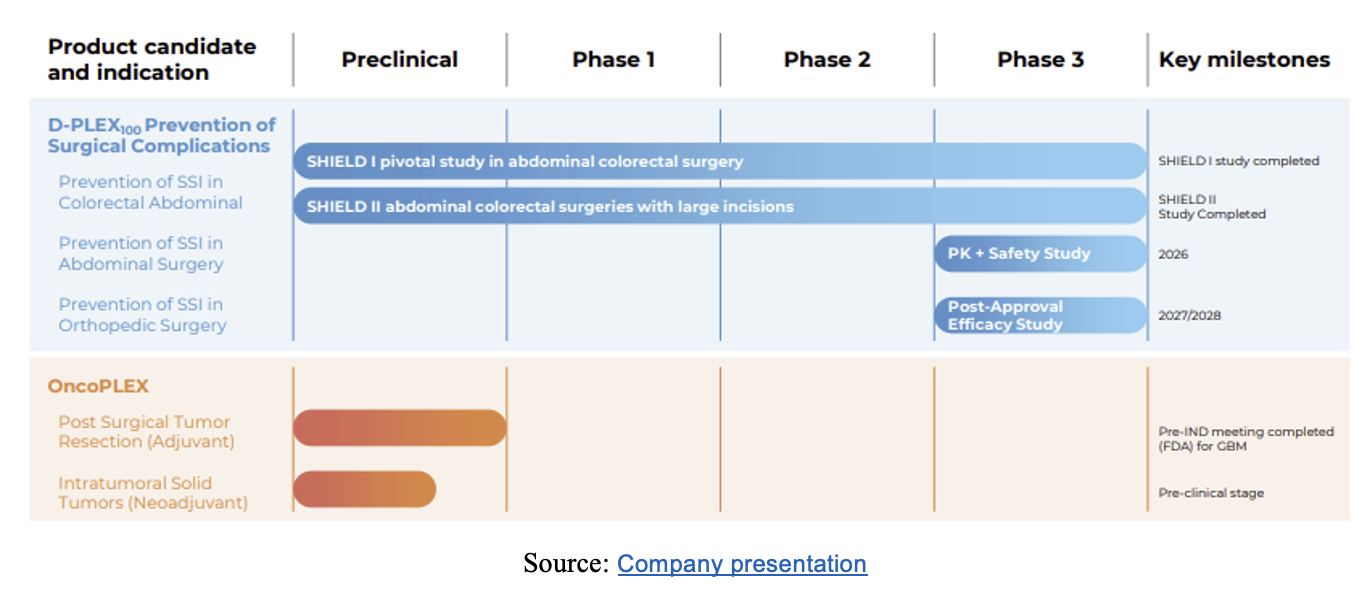

PolyPid intends to submit an NDA (New Drug Application) to the FDA in early 2026 to leverage D-PLEX₁₀₀ Fast Track and Breakthrough Therapy designations and thereby expedite the path to potential regulatory approval. The company also expects to submit a Marketing Authorization Application in the E.U. subsequently.

Importantly, the independent Data Safety Monitoring Board (DSMB) in SHIELD II raised no safety concerns. Earlier, the DSMB had recommended that PolyPid conclude enrollment at the lowest sample size reassessment option, as it believed that would be sufficient to provide statistical significance of the potential positive efficacy of D-PLEX₁₀₀. The company viewed the DSMB’s enrollment recommendation as a positive and believes the study was derisked significantly.

Data expected to facilitate strategic commercial and R&D collaborations to advance D-PLEX₁₀₀

SSI in patients undergoing abdominal colorectal surgery represents a significant post-surgery risk that has been documented to approach 24% in patients with multiple comorbid risk factors, according to research published by the National Institutes of Health (NIH). The company believes the positive results of its SHIELD II Phase 3 pivotal trial demonstrate the ability of D-PLEX₁₀₀ to lower SSI risk significantly and improve clinical outcomes for patients. In addition to improved patient outcomes, there are expected economic benefits, as well. PolyPid believes D-PLEX₁₀₀ could potentially reduce expenses for hospitals and payers and also reduce liability exposure for physicians. The company sees the total addressable market (TAM) in the U.S. alone at more than 12 million annual orthopedic, abdominal, and other surgeries (see below). Based on external third-party data, the company estimates the TAM at launch at more than seven million abdominal surgeries in the combined U.S and European markets.

In 2022, PolyPid formed an exclusive licensing agreement with UK-based ADVANZ PHARMA Corp. for the commercialization of D-PLEX₁₀₀ in Europe. PolyPid is actively pursuing additional partnerships for other markets to enhance the commercial introduction of D-PLEX₁₀₀ and has indicated that it is in advanced discussions with several potential partners to maximize the commercialization of D-PLEX₁₀₀ in the U.S., Canada, China and South America if/when it receives regulatory approval and that SHIELD II topline results have helped advance several ongoing discussions.

Sizable cash infusion followed topline study data

Following the announcement of positive topline data, warrant holders from the company’s recent financing exercised their warrants, generating an incremental $26.7 million in capital for the company. PolyPid anticipates the warrant exercise could extend its cash runway into and beyond the potential NDA application in 2026. Moreover, PYPD also offered a warrant inducement of new warrants at an exercise price of $4.50 per share that could, if fully exercised, lead to an additional capital infusion that management anticipates could extend its cash runway beyond prospective FDA approval of D-PLEX₁₀₀.

Pipeline Extends Beyond SHIELD II Focus

The PLEX platform is flexible and can deliver a variety of therapies, including small molecules, proteins, peptides, and nucleic acids. In addition to studying the efficacy of D-PLEX₁₀₀ in treating abdominal surgery patients, the company also expects to study it for the treatment of patients who require orthopedic surgery. PolyPid also has OncoPLEX in its product pipeline for treatment in oncology patients undergoing surgery and is also exploring licensing opportunities to expand its platform technology and product candidates globally. In addition, PolyPid has entered into an R&D collaboration with ImmunoGenesis to develop novel treatments for solid tumors, leveraging its PLEX technology.

Pipeline with Multiple Near- and Longer-Term Inflection Points

Moreover, PolyPid recently introduced its long-acting GLP-1 receptor agonists (glucagon-like peptide-1 RA) delivery platform designed to subcutaneously release GLP-1 RA for about 60 days, which is significantly longer than current weekly injection regimens. The platform releases GLP-1 in a linear way, overcoming the burst release seen with the current weekly delivered molecules. The company believes this potentially could extend its offering to the treatment of obesity and type 2 diabetes. The World Health Organization (WHO) puts the number of adults living with diabetes globally at more than 800 million, having more than quadrupling since 1990.

Risks

PolyPid faces several risks including the risk that future clinical trials are not successful and do not lead to regulatory approval, that the company will not have sufficient cash to advance its research activities and will have to raise capital that could be dilutive to existing shareholders and that market competition could increase.

SUBSCRIBE TO ZACKS SMALL CAP RESEARCH to receive our articles and reports emailed directly to you each morning. Please visit our website for additional information on Zacks SCR.

DISCLOSURE: Zacks SCR has received compensation from the issuer directly, from an investment manager, or from an investor relations consulting firm, engaged by the issuer, for providing research coverage for a period of no less than one year. Research articles, as seen here, are part of the service Zacks SCR provides and Zacks SCR receives payments totaling a maximum fee of up to $50,000 annually for these services provided to or regarding the issuer. Full Disclaimer HERE.